This is part of our Navigating Net Zero: APAC Climate Guide series. Explore other chapters below.

As one of the world’s biggest financial hubs, Hong Kong is decarbonising its economy by playing to its strengths: finance and technology. These are the ‘dual engines’ powering transformation.

Hong Kong is strategically positioned to influence the shift to sustainable finance and drive investment in green technology and infrastructure. One of the chief advantages Hong Kong holds is its potential to act as a super-connector between Mainland China and the global market. Plans made in late 2024 are set to further grow its green debt market and make it a ‘go-to’ for sustainable financing (find more on the Sustainable Finance Action Agenda below).

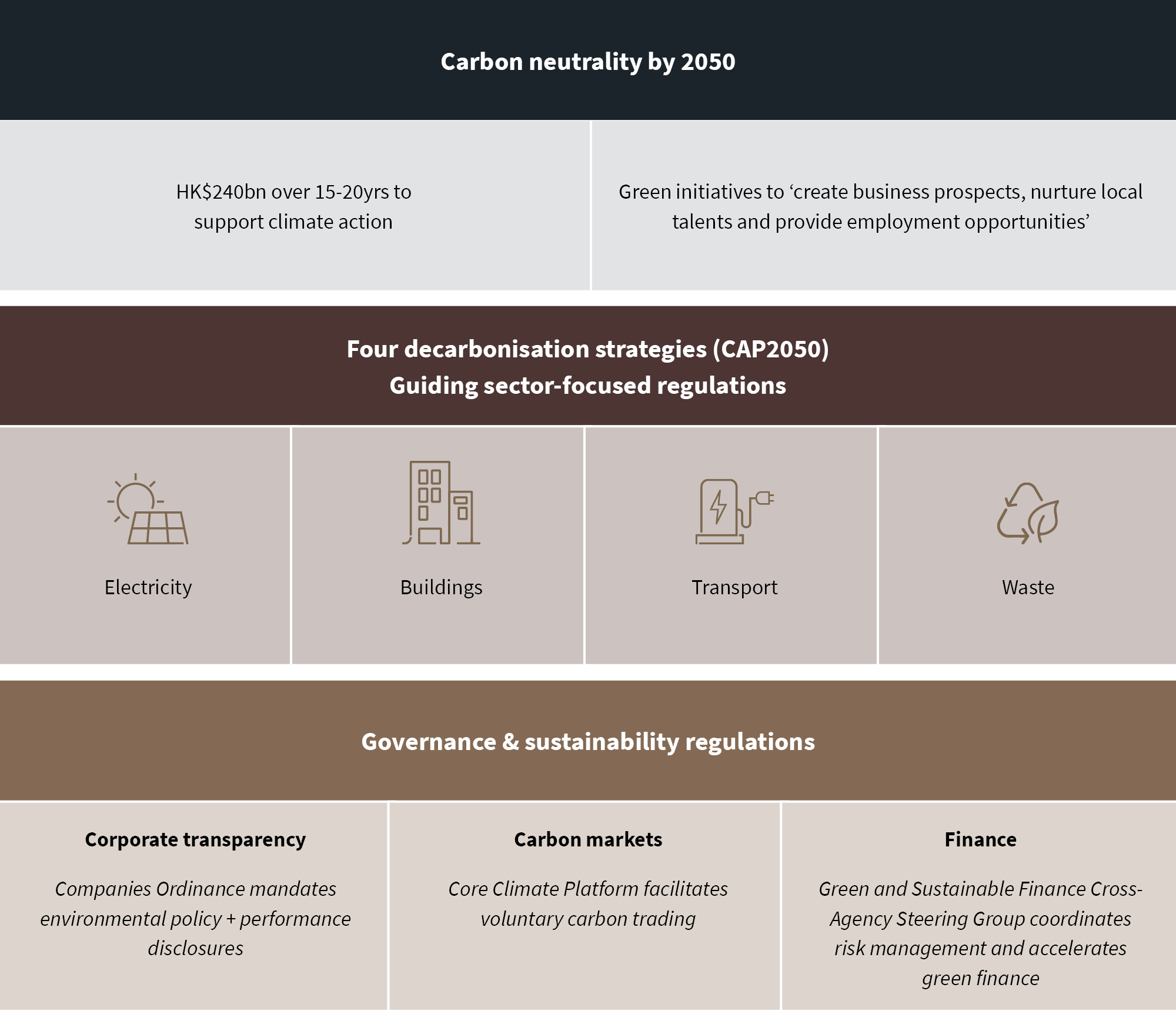

Decarbonisation is prioritised across four key areas in a bid to reach carbon neutrality by 2050: electricity, buildings, transport and waste. A combination of incentives and regulatory requirements encourage businesses to transition. Climate- and sustainability-related disclosures seek transparency and accountability. Hong Kong will also invest HK$240 billion (about US$30.8 billion at time of publication) in climate change mitigation and adaptation measures over 15-20 years, under a policy commitment made in 2021.

The transition to renewable energy sources is complicated by the need for external energy supplies. The city must navigate space constraints and infrastructure limitations, particularly in the adoption of green buildings and transport. And businesses must navigate risks of greenwashing and pressure to meet short-term market demands as they try to reach long-term ESG goals.

Read on for more – and reach out to your KWM Contact.

Challenges persist. Hong Kong’s reliance on fossil fuels for electricity generation – its largest source of emissions - poses a significant hurdle. But public and private sector initiatives to decarbonise the economy are widespread.' — Scott Gardiner, KWM Partner

Download the full publication or click the following to read each section:

Energy Transition | Carbon Markets | Financing | Region Focus: The Greater Bay Area

Download

3.40MB, 24 Pages

Investment opportunities and challenges: Our Top 5

The evolving regulatory and corporate landscape

Hong Kong's regulatory framework for decarbonisation is multifaceted, with several key components working together to cut emissions and promote sustainability.

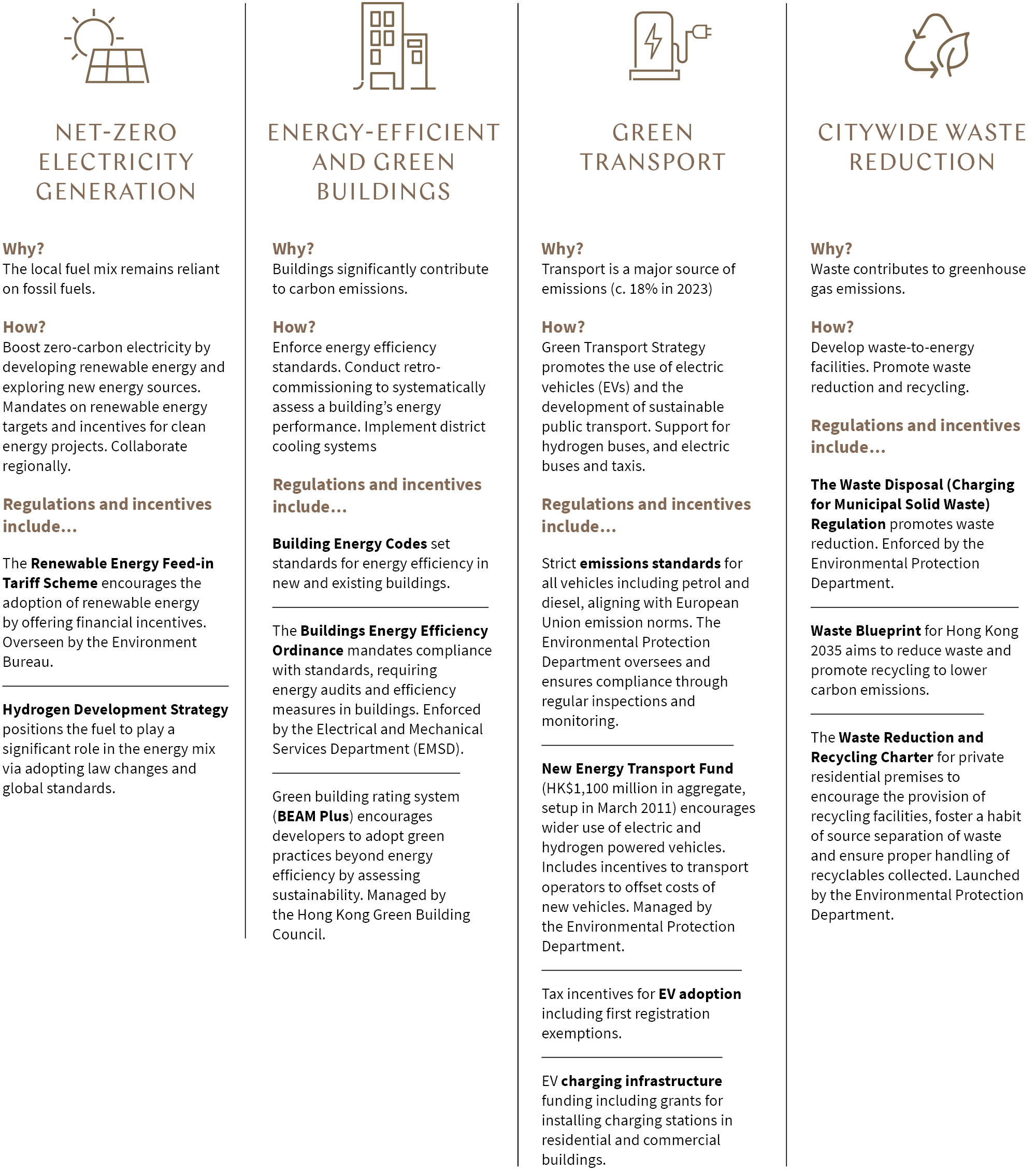

- The Climate Action Plan 2050 (CAP2050) is the regulatory cornerstone, setting the vision for achieving carbon neutrality by 2050. Announced in late 2021, CAP2050 sets decarbonisation targets and pathways to achieve them across four key sectors: electricity, transport, buildings and waste. Each is supported by targeted initiatives and regulations introduced over time (see ‘Energy Transition’ below).

- Efforts to accelerate green finance and co-ordinate climate risk management by the Hong Kong Stock Exchange and regulatory authorities as part of the Green and Sustainable Finance Cross-Agency Steering Group (see 'Financing' below).

- Voluntary carbon trading via the international marketplace Core Climate (see ‘Carbon Markets’ below).

- Corporate transparency measures including environmental disclosures that pre-date CAP2050, various climate disclosures for financial institutions, funds and listed companies, and emerging sustainability reporting measures (see ‘Financing’ below).

These initiatives collectively drive Hong Kong towards a sustainable and low-carbon future, reflecting its commitment to global climate agreements.

For the purposes of the Paris Agreement, Hong Kong’s emissions reduction objective is to reach carbon neutrality by 2050, having already passed its emissions peak in 2014. To ensure alignment, Hong Kong’s objectives sit as an appendix within China’s Nationally Determined Contributions (NDC), registered with the United Nations Framework Convention on Climate Change (note Mainland China’s target is net zero emissions by 2060).

Energy Transition

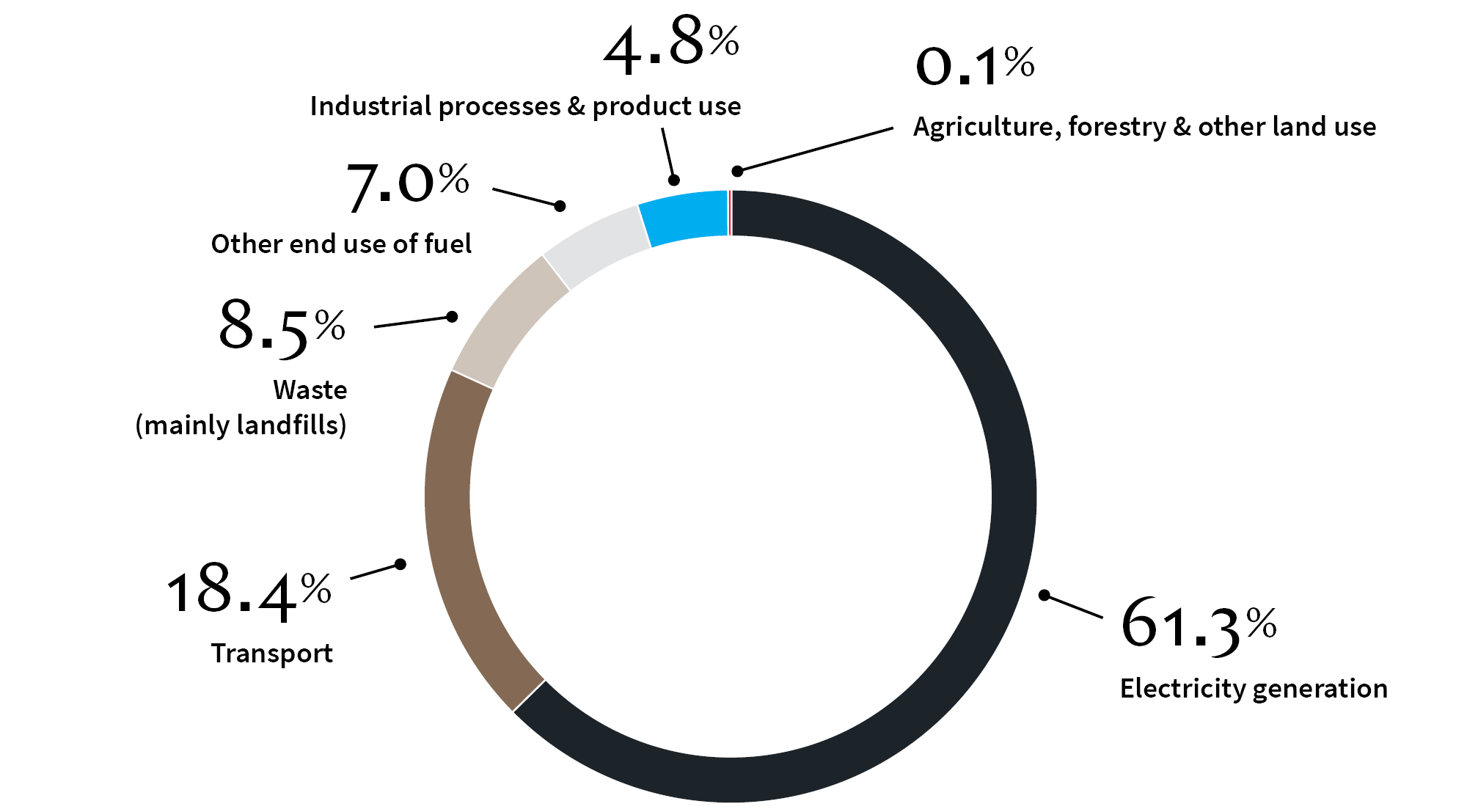

Electricity generation is Hong Kong’s largest source of carbon emissions. Efforts to reduce reliance on fossil fuels are gaining momentum as the government embraces cleaner and more sustainable sources for its future energy mix. This includes hydrogen, nuclear and natural gas. Energy efficiency is a priority, given urban density, as is expanding EV infrastructure.

Renewables have played a relatively minor role in the energy mix to date (less than 1% of electricity generation in 2022 according to the IEA). This is set to change under CAP2050. Government-led projects combined with incentives to encourage private investment (including feed-in tariffs) are expected to grow the share to 7.5-10% by 2035.

Collaboration is key – including through local projects, regional cooperation and joint ventures. The roll-out of solar systems across government offices, schools and other facilities, and installation of waste-to-energy and hydro power systems at sewage treatment plants are among examples of how the government is actively working – as it notes in CAP2050 – to ‘grapple with Hong Kong’s geographical and environmental constraints in driving the development of renewable energy’.

Source: Hong Kong Greenhouse Gas Emissions by Sector in 2023

Significant steps taken to diversify and stabilise energy include:

- Importing nuclear energy, cutting more than 7.5 million tonnes of CO2 emissions per year (in 2023 total emissions were 34.5 million tonnes CO2 equivalent)

- Developing Hong Kong’s first offshore LNG terminal (entered into service July 2023, jointly developed by Hong Kong's electricity providers CLP Power and HK Electric)

- Launching Hong Kong’s first EV as a Service, a one-stop EV rental and charging service (May 2023 by CLP Power and AVIS).

Regulatory settings and government efforts to encourage change

The Hong Kong government’s ambitious targets for energy transition are set out in its CAP2050 plan (detailed in the Jurisdiction Snapshot above). Critically, this includes an overarching pledge to cease using coal for daily electricity generation by 2035, leaving it as a backup source only. Some 60-70% of energy will come from carbon-free sources.

How renewable energy certificates are motivating the market

Hong Kong's electricity sector is privately-owned and operated by two electricity providers - CLP Power Hong Kong Limited and The Hongkong Electric Company Limited. The Hong Kong Government monitors the performance of the power companies through the Scheme of Control (SoC) Agreement. To promote the development of renewable energy under the SoC arrangements:

- non-governmental bodies or individuals who install solar or wind energy generation systems at their premises can sell the renewable energy they generate to the power companies at a rate higher than the normal electricity tariff rate under the Feed-in-Tariff scheme.

- any residential or commercial and industrial customers can purchase renewable energy certificates from their supplier (CLP Power or HK Electric) which represent the environmental attributes of electricity produced by local renewable energy sources (including solar power, wind power and landfill gas projects). Each renewable energy certificate is priced at a premium to the top of the normal price of a unit of electricity. The current pricing (as at March 2025) is HK$0.5 per unit of electricity, for a minimum of 100 units. This is reviewed annually to reflect market demand.

Hydrogen as a future fuel for Hong Kong

Seizing the opportunities brought about by the development of hydrogen energy can help Hong Kong strive towards carbon neutrality, develop a new quality productive force and maintain international competitiveness.' – Secretary for Environment and Ecology, Mr Tse Chin-wan

One of the more significant regulatory efforts by the Hong Kong government in its bid to transition to clean fuel relates to hydrogen. The Hong Kong government announced the Strategy of Hydrogen Development in June 2024. Critical objectives include:

- Legislative amendments by mid-2025 to regulate using hydrogen as a fuel (including manufacturing, storing, transporting and using hydrogen)

- Certification approach by 2027, for a hydrogen standard aligning with international practices

- Facilitating regional cooperation and investment through joint ventures

- Promoting opportunities with Mainland and foreign businesses.

Hong Kong makes it clear in its strategy: it must stay flexible, given uncertainty around whether green hydrogen costs will become competitive.

For more on the evolving role of hydrogen – in Hong Kong and beyond – visit KWM Pulse.

What role can the private sector play?

The private sector plays a crucial role in Hong Kong's energy transition. Hong Kong's strategic position as a financial hub enables it to attract investment and foster collaboration. Opportunities for involvement include:

- Green bonds and sustainability-linked loans

Financial institutions are developing innovative green finance products, supporting sustainable projects and technologies (see ‘Financing’ below for more details).

- Corporate Power Purchase Agreements (PPAs)

Large corporations in Hong Kong can directly purchase renewable energy, driving demand and supporting project development.

- Hydrogen energy technologies

With Hong Kong's focus on hydrogen, companies can engage in developing technologies related to hydrogen production, storage and utilisation.

- Renewable energy project development

Companies are investing in clean energy projects, such as solar PV systems and wind turbines, to reduce emissions.

- Construction and retrofitting

The real estate sector is leading the way with green building designs and retrofitting projects that enhance energy efficiency.

We need to talk about (green) buildings

Since 1990, Hong Kong has had an urban population of 100% - almost double the global average based on World Bank data. The undeniably urban landscape is dotted with skyscrapers – more than any other city in the world according to Council on Tall Buildings and Urban Habitat data.

This helps to explain why Hong Kong’s buildings consume about 90% of electricity and emit 60%+ of carbon. The global average for buildings is closer to a third of energy consumption and 26% of carbon emissions.

Hong Kong is trying to change that.

Various programs and policies encourage the adoption of sustainable building designs and green technologies. Examples include automatic demand control of chilled water circulation systems, control of fresh air supply with carbon dioxide sensors, greenery to reduce heat and air-cooled chiller plants with AI optimisation controls.

- The Hong Kong government is preparing to amend the Building Energy Efficiency Ordinance (BEEO) to include more types of buildings, mandate disclosure of energy audit report information and shorten the interval of energy audits.

- The Energy Efficiency Registration Scheme was introduced to recognise buildings which outperform the statutory requirements of BEEO.

- The Hong Kong Green Building Council launched its Climate Change Framework for Built Environment in June 2023, providing a practical reference point for the industry and building owners to embark on their net zero journey.

- Public housing blocks are undergoing refits with flexible PV systems (30 since March 2024), and all the Housing Authority’s new buildings are designed to meet the assessment criteria of the HKGBC’s BEAM Plus, aiming for gold rating standard or above.

- District Cooling Systems are increasingly incorporated into new development areas.

Carbon Markets

Hong Kong aims to become a regional carbon trading hub and regional super-connector between global investors and Mainland China. And it is well-positioned to get there, as a global financial centre with a robust regulatory framework, international investor base and understanding of markets in Mainland China.

Although Hong Kong lacks a compliance carbon market and does not participate in Mainland China's, its voluntary market is robust. It also boasts a marketplace that connects international investors with opportunities in the region: HKEX’s Core Climate platform. Hong Kong aims to build a dynamic regional carbon marketplace and is working with neighbouring cities to develop a sustainable carbon market in the Greater Bay Area (GBA).

Strategic collaborations including HKEX signing Memoranda of Understanding with the China Emissions Exchange (Guangzhou) and the China Emissions Exchange (Shenzhen) to promote sustainability through carbon finance, including to explore the development of a voluntary carbon emission reduction programme.

These developments are strengthening Hong Kong's position as a regional hub for carbon trading and sustainable finance.

To see a timeline of the significant shifts over the past decade and upcoming regulatory dates, visit our Carbon Markets Regulatory Tracker for Hong Kong.

Voluntary carbon market - HKEX Core Climate

HKEX’s Core Climate is intended to build an integrated ecosystem and international carbon market in Hong Kong, to provide a one-stop solution for trading, custody and settlement. It connects capital and international investors with climate-related products and opportunities in Hong Kong, Mainland China and beyond.

Core Climate is currently the only carbon marketplace that offers Hong Kong Dollar and Renminbi settlement for the trading of international voluntary carbon credits.

All projects available on Core Climate are verified against international standards, including Verra and the Gold Standard. To allow a more diverse range of internationally certified climate projects, HKEX included the Gold Standard’s Verified Emission Reductions (effective on 1 August 2024), a form of carbon offset that can be traded on the voluntary market for carbon credits.

There are no licensing requirements for trading carbon credits through Core Climate, unless the units or derivatives constitute securities – in which case they are regulated by the Hong Kong Securities and Futures Commission (SFC).

In recommendations released late last year, a government advisory body set a path to enhancing Hong Kong’s role as a leading financial centre. The systemic changes recommended would complement Core Climate and help stimulate demand and build a vibrant ecosystem for carbon trading. See the 'Regional Focus' section on the Greater Bay Area below for details.

Super-connector potential: Hong Kong's role in Mainland China’s growing carbon market

'By providing connectivity for international investors to onshore markets, and vice versa, Hong Kong could play a super-connector role linking carbon projects with investors looking to drive the low-carbon transition and allocate capital to green and sustainable finance projects. The development of a carbon market would also inject new vitality to the development of green finance in Hong Kong.’ – HKEX, The growth of global carbon markets and opportunities for Hong Kong 2023

The Financial Services Development Council (FSDC) of Hong Kong has outlined a strategic vision to leverage Hong Kong’s financial clout and geographical advantage. In December 2024 it released ‘Internationalising China’s Carbon Market: The Role of Hong Kong as an International Financial Centre’. Noting the Mainland market was ‘gaining momentum’, the FSDC highlighted the ‘untapped potential’ for Hong Kong to become a go-to carbon trading destination, with voluntary carbon markets expected to grow to US$10.3 billion in Mainland China and US$10-40 billion in the rest of the globe by 2030.

Aiming to address barriers such as limited international recognition and investor access, the FSDC recommends short and medium term practical actions:

1. Stimulate demand for carbon credits.

2. Set up ‘Carbon Connect’ for cross-border trading.

3. Create a non-governmental carbon registry for international credibility.

4. Clarify legal standing of carbon credits.

5. Build a vibrant ecosystem with solid professional services and technology.

The FSDC's recommendations enhance the environment in which Core Climate, Hong Kong’s carbon marketplace, operates. They aim to make Hong Kong the go-to destination for carbon trading, leveraging the existing strengths of platforms like Core Climate.

These measures promise to boost Hong Kong's influence in the global carbon market and support its sustainability efforts, particularly in the GBA (see 'Regional Focus' below for more on the significance of this).

‘By stimulating demand for carbon credits, setting up a cross-boundary trading channel, establishing a carbon registry, providing greater legal certainty for carbon credits, and developing a vibrant carbon market ecosystem supported by advanced technologies, Hong Kong would be well equipped to support the internationalisation of Mainland China's carbon market.’ – FSDC Policy recommendations, Dec 2024

The HKEX has teamed up with the China Beijing Green Exchange with a clear goal: promote sustainable finance, build an ESG ecosystem and drive green development within the Belt and Road Initiative.

A Memorandum of Understanding signed by both exchanges in November 2023 sets out the agreement to collaborate on research and opportunities. The China Beijing Green Exchange manages the Chinese national voluntary greenhouse gas emission reduction trading system.

This follows HKEX's earlier partnership with the China Emissions Exchange in Guangzhou, signed in March 2022. The China Emissions Exchange provides a platform for renewable energy assets and environmental commodity products (such as emission allowances). Their shared mission is carbon finance, providing trading options for renewable energy and emission allowances — a marketplace for clean initiatives.

These agreements help companies in the region cut their carbon footprints and adopt cleaner technologies. The initiatives make the GBA a leader in climate-conscious development, contributing to a sustainable future, and help achieve interconnection between the carbon market and international markets.

Financing

Plans to make Hong Kong the ‘go-to’ for sustainable financing in the region and beyond are part of the Sustainable Finance Action Agenda launched by the Hong Kong Monetary Authority (HKMA) in October 2024. This bold move builds on Hong Kong's ongoing efforts to expand its green and sustainable debt market.

A new taxonomy to support sustainable investments, along with plans for sustainability disclosures consistent with international standards, are setting frameworks to strengthen Hong Kong’s hub status.

Hong Kong is also due to release a Green Fintech Map, a directory of green fintech firms operating in Hong Kong, highlighting its focus on innovation. The Prototype Hong Kong Fintech Map was launched in May 2024.

A key impetus behind these developments was the formation of the Green and Sustainable Finance Cross-Agency Steering Group (Steering Group) in May 2020. The Steering Group, initiated by the SFC and HKMA, brings together government bureaus, regulatory authorities and the Hong Kong Stock Exchange with a joint mission of accelerating green finance.

In addition, the Green Technology and Finance Development Committee was set up in June 2023 to help build an action agenda for promoting the development of Hong Kong into an international green technology and finance hub.

The Hong Kong Government has also introduced a range of schemes, making billions available to support both public and private sustainable finance initiatives.

- Sustainable government projects - up to HK$500 billion

The Government Sustainable Bond Programme (renamed May 2024, previously the Government Green Bond Programme) authorises the government to borrow to fund sustainable projects (via the Capital Works Reserve Fund).

- First-time issuers of green and sustainable bonds – up to HK$2.5 million issuance and HK$800,000 review costs per instrument

The Green and Sustainable Finance Grant Scheme (administered by HKMA) subsidises the issuance and review costs of green bonds and loans, encouraging a wider range of industry players to enter the market.

- Green tech developments - HK$400 million allocated to GTF

The Green Tech Fund encourages cutting-edge developments, backing and approving 33 projects to date, involving a total grant of around HK$147 million. These range from green hydrogen production and construction materials, to noise-absorbing meta-materials using recycled plastic.

- Early-stage funding – up to HK$150,000 per project

The Green and Sustainable Fintech Proof-of-Concept Funding Support Scheme (launched June 2024) funds technology companies and research institutes to collaborate with local enterprises to co-develop innovative new projects.

- Training for practitioners - HK$200 million

Subsidies to local eligible and prospective practitioners participating in training related to green and sustainable finance – available since 2022 under the Pilot Green and Sustainable Finance Capacity Building Support Scheme.

Hong Kong’s financial market is also among the most innovative. Marking an important milestone for Hong Kong in combining green finance and fintech, the Hong Kong Government successfully issued two batches of digital green bonds in recent years: the world’s first tokenised government green bond in February 2023 and the world’s first multi-currency digital bond in February 2024.

For the groundbreaking tokenised green bond, the government issued HK$800 million under its Global Medium Term Note Programme.

This pilot initiative marked a pioneering use of distributed ledger technology. The bonds, with a 4.05% interest rate and a one-year tenor, were recorded in tokenised securities accounts, and payments made via cash tokens linked to the HKMA.

A crucial test of Hong Kong’s financial infrastructure and market practices, aligning with global trends in sustainable finance and market digitalisation.

The Steering Group, co-chaired by the HKMA and SFC, coordinates the management of climate and environmental risks to the financial sector, accelerates the growth of green and sustainable finance in Hong Kong, and supports the government’s climate strategies. The Steering Group launched the Centre for Green and Sustainable Finance to coordinate cross-sector efforts on capacity building and data.

The Steering Group has set three priorities for 2025:

- Sustainability disclosures: Developing a comprehensive ecosystem based on a roadmap released by the Financial Services and the Treasury Bureau, towards the full adoption of the International Sustainability Standards Board (ISSB) Sustainability Disclosure Standards by 2028. This will put Hong Kong among the first jurisdictions to align its local requirements with the ISSB Standards.

- Transition finance: Expanding the Hong Kong Taxonomy to incorporate transition and new activities.

- Data solutions: Releasing a Green Fintech Map to find solutions to increase data availability (including emissions calculation tools) and support reporting.

Climate disclosures have been a focus for the Steering Group more broadly since its inception. Various efforts by the HKMA, HKEX and SFC are detailed in ‘Disclosure and reporting’ below.

How HKMA is building Hong Kong’s hub status

The HKMA released an ambitious Action Agenda in October 2024, detailing eight goals to help ‘consolidate Hong Kong’s position as the sustainable finance hub’:

Targets for banks

1. Strive to achieve net zero in operations by 2030 and financed emissions by 2050

2. Enhance transparency on climate-related risks and opportunities

HKMA’s investments

3. Achieve net-zero emissions for the Investment Portfolio of the Exchange Fund by 2050

4. Support transition in the region through investment

Hong Kong as a hub

5. Develop Hong Kong into the go-to sustainable financing platform of the region and beyond

6. Catalyse innovation in sustainable finance

Inclusive finance sector

7. Support high-quality and comprehensive sustainability disclosures

8. Close talent and knowledge gaps in sustainable finance in the region

Greening Hong Kong’s banks and financial sector

The net zero and transparency goals set for banks as part of its Action Agenda are simply the latest in a stream of initiatives by the HKMA in recent years to ‘green’ the finance sector.

Among its earliest and most significant moves to transform banks was the 2020 co-launch of the Alliance for Green Commercial Banks with the World Bank’s International Finance Corporation. The global initiative aims to mainstream and scale up green and sustainable finance in commercial banking, sharing practical solutions. Bank of China (Hong Kong), Citi, Crédit Agricole CIB, HSBC and Standard Chartered are the Cornerstone Banks.

Various HKMA initiatives support and accelerate the shift, including:

- Integrating climate risk into supervisory processes, under a two-year plan to build climate resilience into the banking system (Supervisory Policy Manual (SPM) module GS-1 on ‘Climate Risk Management’ issued December 2021). In addition, tentatively from 2030, banks are expected to start making available their transition plans to the HKMA regularly on a ‘comply or explain’ basis.

- Enabling banks to assess the potential impact of physical risks on residential and commercial buildings in Hong Kong under different climate scenarios, via a cloud-based Physical Risk Assessment Platform. This comprises an analytical tool gives users access to 40+ public data and data sources related to physical risk.

- Integrating ESG factors into the investment process of the HKMA’s Exchange Fund. This has the added benefit of ‘leading by example’.

Encouraging listed companies and issuers to decarbonise

Regulations and guidelines encourage listed companies and issuers to embrace green and sustainable finance. Highlighting Hong Kong’s vast potential as a gateway to the region, HKEX is currently the largest listing venue for Chinese offshore green bonds.

- Regulatory framework: The SFC is committed to developing an effective regulatory framework for green finance in Hong Kong. It published the Agenda for Green and Sustainable Finance in 2022 to set out further steps to support Hong Kong’s role as a regional green finance centre. This focuses on corporate sustainability disclosures, monitor implementation of sustainable finance measures and regulatory framework for carbon markets.

- Guiding the transition: The HKEX published a practical guide to help companies develop a pathway to net zero in December 2021 (Practical Net-Zero Guide for Business).

- Educating players: The HKEX runs a centralised education platform to support listed issuers, known as the ESG Academy.

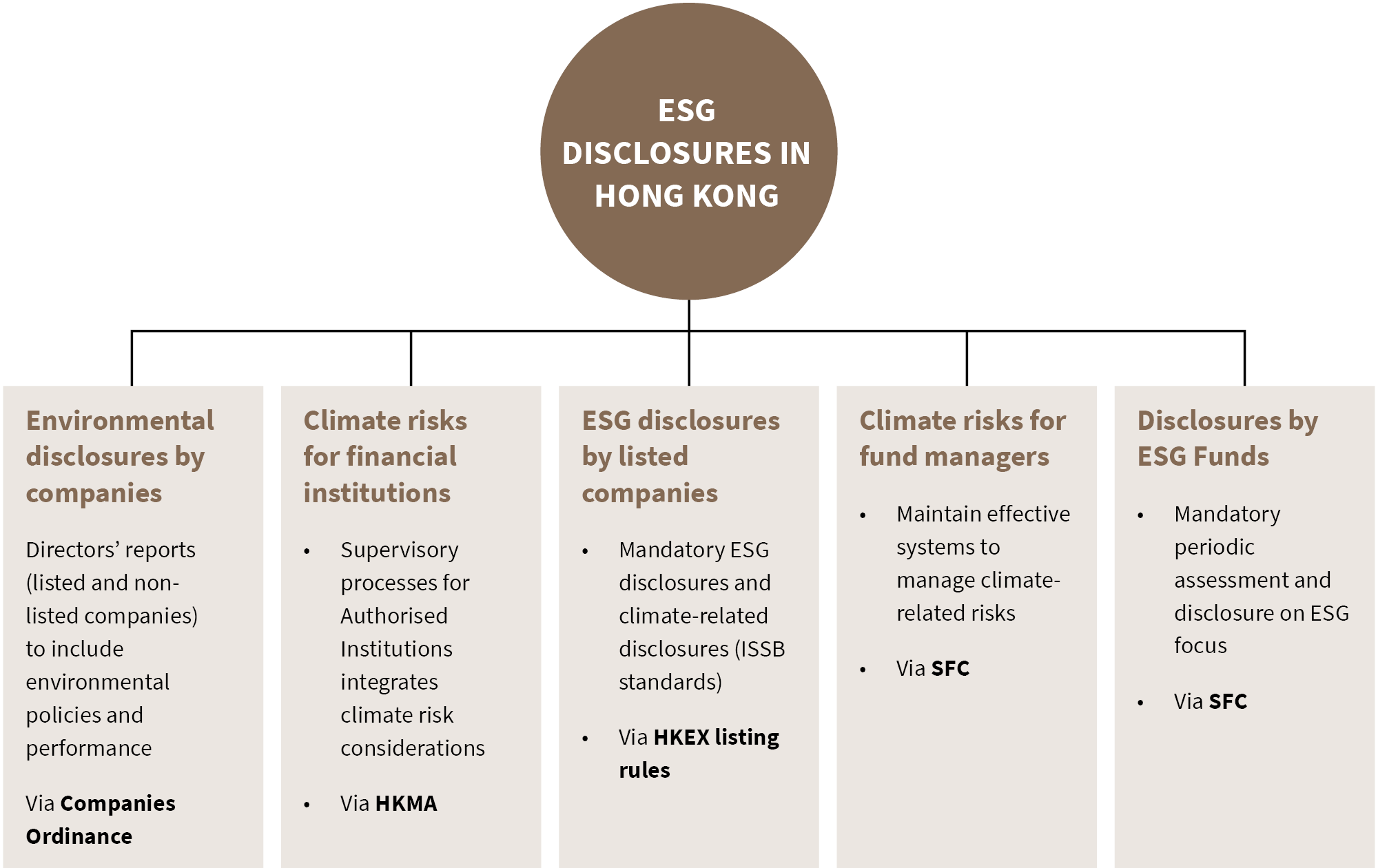

Disclosure and reporting

Regulatory Landscape For Disclosure in Hong Kong

Climate and sustainability related disclosures have rapidly evolved in Hong Kong, with more developments on the way in a bid to boost transparency and accountability, encourage responsible investment and promote a greener economy.

Existing and emerging measures include…

HKEX Listing Rules requiring:

- For all listed companies, mandatory ESG disclosures and climate-related disclosures (ISSB standards)

- For LargeCap Issuers, climate-related risks and business model and strategy climate resilience (ISSB S2 standard). Those with a material presence in Hong Kong will likely need to clearly articulate their mitigation efforts to attract capital going forward.

- From 2025, on a ‘comply or explain’ basis

- From 2026, mandatory

Keeping it transparent – and accessible

Investors and asset managers have easy access to these ESG metrics through an online portal known as STAGE (provided by HKEX in partnership with leading ESG data providers). This provides information on a wide range of sustainable, green and social investment products, helping issuers increase the visibility and awareness of their sustainable financial products.

Securities and Futures Commission requirements for:

- Fund managers to make climate-related disclosures and factor climate-related risks into their investment and risk management processes (Fund Manager Code of Conduct as amended in October 2024)

- ESG Funds to follow enhanced and ongoing disclosure requirements. If ESG factors are the key investment focus, this must be reflected in the investment objective and/or strategy (Set out in the ‘Circular to management companies of SFC-authorised unit trusts and mutual funds – ESG funds’).

Mandatory Provident Fund Authority requirements for:

- Mandatory Provident Fund (MPF) trustees to integrate ESG factors into investment and risk management, and to make relevant disclosure to MPF scheme members.

Insurance Authority requirements for:

- Insurers to consider climate risks (and other material risks) as part of their ‘enterprise risk management’ frameworks.

The Hong Kong Taxonomy for Sustainable Finance, published by the HKMA in May 2024, aims to raise awareness of green finance, promote understanding of green activities and facilitate green finance flows. While it is voluntary, the HKMA encourages banks to use the taxonomy when labelling or assessing investments, as well as in making disclosures.

Aiming for interoperability, the Hong Kong Taxonomy was developed with other taxonomies in mind, including the Common Ground Taxonomy (which compares EU and China’s taxonomies) and the ASEAN Taxonomy.

There are 12 economic activities covered across 4 sectors: power generation, transportation, construction, and water and waste management (as at March 2025). This is due to expand to include more sectors and activities (including transition activities), with the taxonomy described as a ‘living document’.

Region Focus: The Greater Bay Area

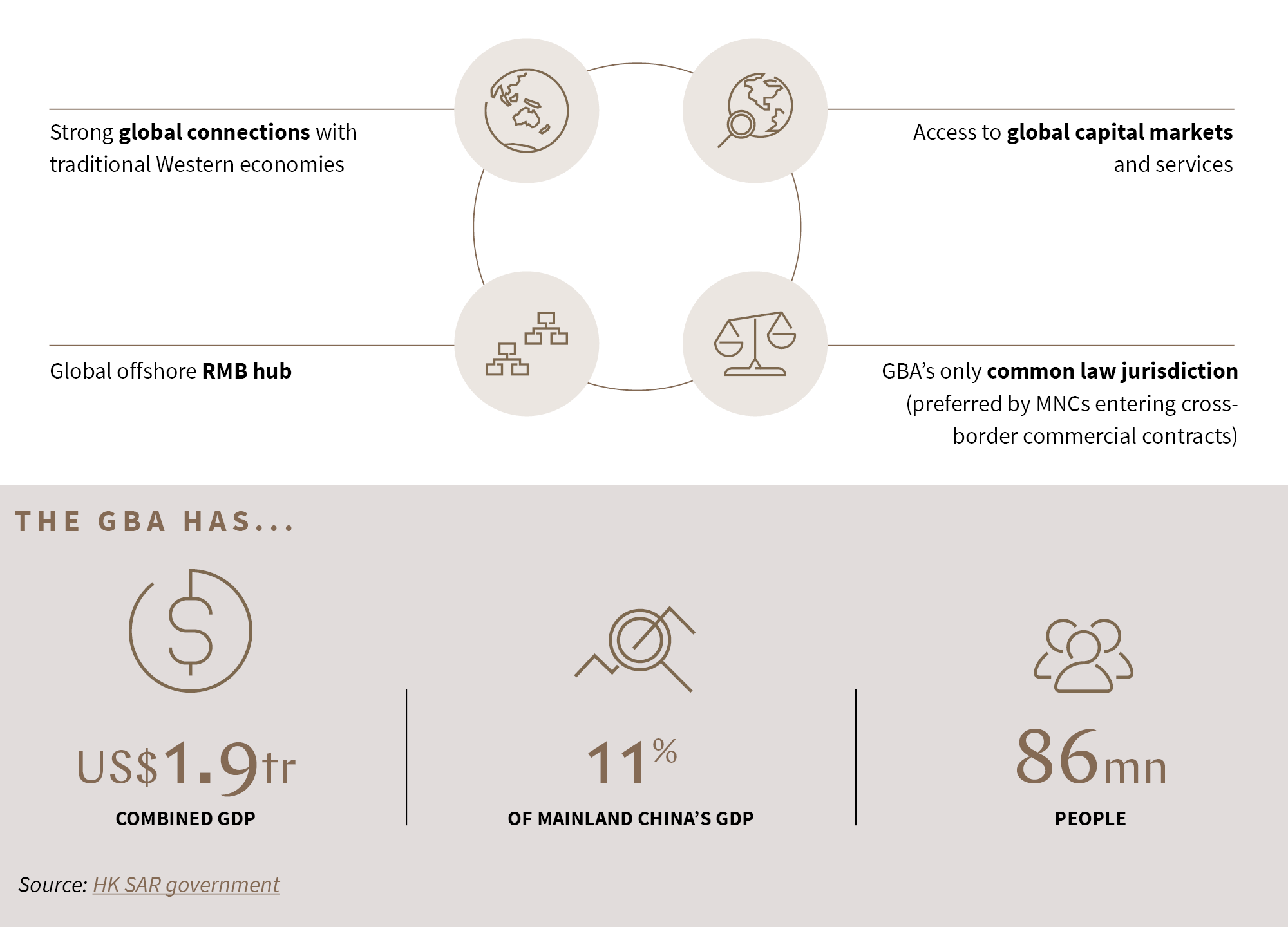

If the Greater Bay Area (GBA) is viewed as a single economic state, its GDP of ~USD1.9 trillion would rank it within the top twelve globally, ahead of Australia and Indonesia. Emerging from China’s vision to transform the Pearl River Delta into a powerhouse of innovation and economic growth, the GBA brings together Hong Kong, Macao and nine municipalities in Guangdong Province.

This dynamic economic hub with a population of over 86 million presents unique business and investment opportunities. And Hong Kong, as a financial centre, is strategically positioned to drive green finance and technology integration within the GBA. From channelling investments into sustainable projects across the region and enhancing market liquidity, to connecting with Mainland China's carbon markets, Hong Kong plays a crucial role.

Advanced settings in bonds, insurance and mortgages, capital market connections and integrated service offerings are among Hong Kong’s strengths that will play to its advantage as the GBA grows.

A range of measures – both in place and proposed – are set to boost Hong Kong’s influence in the global carbon market and support sustainability efforts in the GBA and beyond.

Hong Kong's Role in the GBA: Unique Advantages

Five ways Hong Kong is encouraging and improving collaboration in banking and finance across the GBA

The GBA is not just a region. It’s a vision for the future, with Hong Kong leading the charge as a hub for innovation and investment. We’re watching closely – and involved in numerous projects – as the region develops. Here are five banking and financial sector developments that are opening opportunities.

Located in the Lok Ma Chau Loop, the 87.7 hectare Hong Kong-Shenzhen Innovation and Technology Park is a hub for tech innovation. It offers opportunities for startups and tech companies to collaborate and grow, across six pillar industries including AI & data science, robotics and new energy. It harnesses talents from both Shenzhen and Hong Kong.

But more than that, there is a sustainable drive behind its efforts. The park is designed with a smart and green approach and commits to achieving net-zero by 2045. This includes reusing water, adopting renewable energy and installing EV chargers.

In this guide, references to ‘Hong Kong’ are references to the Hong Kong Special Administrative Region of the People’s Republic of China, and references to ‘China’, the ‘Mainland’, ‘Mainland China’ or the ‘PRC’ are references to the People’s Republic of China excluding Hong Kong, the Macau Special Administrative Region and Taiwan.

Discover the trends shaping tomorrow's markets. Stay ahead in Asia.