Our new APAC Data Centre Regulatory Guide unpacks what you need to know about one of the most significant investment asset classes globally.

- Read on for 8 themes to watch and our regulatory heatmap

- Jump to the end to navigate the settings in 13 jurisdictions, from Australia to Vietnam

- You can also download the Guide in full below

Harnessing data centre opportunities across the APAC region without 'hype-crash' risk requires sectoral intelligence.

The APAC region has experienced a significant portion of data centre growth in a trend that is set to accelerate. The region is expected to require 1.7 times the capital of the US to develop its pipeline. Local development opportunities are evolving, as cloud service providers and enterprises increasingly build capacity in-country instead of operating from regional gateways. This is creating opportunities for investors to build and operate data centres in jurisdictions with traditionally low capacity.

60% of the world’s population resides in the APAC region, where economies are rapidly growing, modernising and digitalising.

Yet regulatory requirements across the APAC region vary and can be opaque. In some cases, there is a perception of having to take ‘sovereign risk’ when investing in emerging economies.

This Guide shares the 8 key themes you need to know about the APAC market and a 'regulatory heatmap'.

In addition, it contains detailed jurisdictional snapshots for 13 key markets , compiled in collaboration with local firms across the region: ABNR (Indonesia), Chandler Mori Hamada (Thailand), Frasers Law Company (Vietnam), Kim & Chang (South Korea), Romulo Mabanta Buenaventura Sayoc & de los Angeles (Philippines), Skrine (Malaysia), Trilegal (India) and Tsar & Tsai Law Firm (Taiwan China). We are enormously grateful for their help.

For a deeper dive into any of these key markets, contact one of our experts. We can provide tailored advice on how to navigate

the regulatory challenges.

What you'll find in this guide

The regulatory landscape - laws, policies, market practices - relating to:

Understanding the diverse markets of the APAC region - at a deep, local level - is critical for participating in the phenomenal data centre growth story that is unfolding. This Guide is designed to help. We're thrilled colleagues from 13 key markets could join us to bring these insights to you.” - KWM Partner Daryl Cox

Key regulatory themes to navigate

From power availability to AI sovereignty, this Guide highlights several important regulatory trends for data centres. Mapping and navigating them is essential for sustainable investments and operations in each market.

Here are our 8 themes to watch. For further detail on the themes in each market, please see the local jurisdictional snapshots.

Data centres require more power and its availability is a critical enabler across all markets

The availability of stable and reliable power is a decisive factor for selecting data centre sites across APAC. As data centres scale up to meet the demands of cloud computing and generative AI, power requirements have increased, making energy availability a major bottleneck across all markets.

The power challenge persists

Even before recent data centre growth, many jurisdictions encountered issues with the stability and availability of their electricity grid.

Governments in all jurisdictions are now having to balance market demand for more data centres (and their associated power load) with competing objectives, such as electrification of daily activities and decarbonisation of the energy industry.

Governments are responding (but approval and connection times are still long)

In both developed and developing markets across the region, government or grid operator approvals for data centre projects focus on the existing grid to service new data centres. Many jurisdictions have a requirement to undertake a power impact assessment before a connection request is granted. This can increase lead times for approvals and, from a developer’s perspective, complicates the site selection and acquisition process.

Fast approvals and innovative approaches are appearing

Depending on the location, sites in emerging jurisdictions such as India, Vietnam and Indonesia may get approved faster, in some cases within a few months. However, timelines will vary from location to location within each jurisdiction based on the extent of power distribution infrastructure available.

With these constraints, some governments are encouraging the development of new data centres away from populated areas and closer to power generation.

For example, Japan’s Ministry of Economy, Trade and Industry offers financial incentives to develop facilities away from Tokyo and Osaka.

In South Korea, there is increasing pressure to move data centre capacity closer to the generation on the East coast (where the bulk of the nuclear generation capacity is located).

WHAT YOU NEED TO CONSIDER

- Assess power sources for your demand – evaluate availability of grid capacity and alternative sources, time to procure, cost and sustainability.

- Evaluate connection timeline – consider innovative approval pathways, but build in realistic project timeline, with alternatives options, including different sites, power sources and use cases.

- Assess if the operator can implement power sharing, hedging or other arrangements to manage demand, and assess regulatory impact.

Going ‘green’: APAC is on the move, and many investors demand it

All markets covered in this Guide have ratified the Paris Agreement and the Kyoto Protocols, making commitments to reduce carbon emissions.

However, these international commitments generally do not translate into regulatory requirements on data centre developers and operators to ‘go green’. This is despite the outsized consumption of energy and water by data centres.

Instead, there is a focus on power usage effectiveness (PUE) as a metric to gauge the sustainability of data centres, with several jurisdictions imposing targets or mandatory limits on PUE for new data centres:

- Singapore – the DC-CFA scheme requires a PUE of 1.3 or lower

- Vietnam – a target PUE of 1.4 or lower

- Japan – planning approvals require a PUE of 1.4 or lower by 2030

- Malaysia – a target PUE of 1.4 or lower for hyperscale data centres

- China - data centres for government require a PUE of 1.3 or lower.

WHAT YOU NEED TO CONSIDER

- Lean into the ‘green’ opportunities where local policy and capacity align (for example, renewable power sources, sustainable cooling, or innovative tech). Explore corporate PPAs to secure renewable energy sources.

- Monitor PUE regulations and targets to maintain compliance and improve sustainability.

- Consider investor pressures and global trends towards sustainability in decision-making processes.

Water: keeping our cool

Data centre IT equipment generates an incredible amount of heat and requires constant cooling to maintain an operating temperature, and to avoid outages.

While power has taken centre stage for regulatory intervention across the markets discussed in this Guide, water usage is emerging as a growing area of focus.

Water availability is a pressing concern, especially in Australia and parts of Indonesia and Malaysia. Innovative cooling systems, such as using recycled water or advanced air or liquid cooling technologies, are gaining traction. These measures not only address environmental concerns but also drive operational efficiency.

Improved water efficiency is a major focus of innovation efforts for data centre operators and the supply chain that supports them. For example, liquid cooling systems have emerged to cool high-performance chips such as GPUs. These are closed loop systems, which can reduce the amount of water that evaporates, increasing water efficiency.

In several markets, planning authorities consider how a data centre operator plans to incorporate water-efficient systems into its operations when assessing an application for planning approval.

Data centres are not alone in demands for water

For many jurisdictions in this Guide, particularly in Southeast Asia, agriculture remains an important economic sector that is also dependent on access to large amounts of water.

Governments in those jurisdictions have competing water policy demands as they seek to encourage data centre investment (often to support policies of digitisation and economic development) without undermining the agricultural sector that sustains their export economies. Addressing these policy tensions is important when seeking approvals to build data centres in the region.

WHAT YOU NEED TO CONSIDER

- Check compliance with any water rights grants and licensing frameworks, and assess additional steps to be factored into project timetables. Engage with planning authorities early.

- Consider implementing water-efficient cooling systems in data centre designs, and procuring water from alternative sources.

- Assess local water scarcity issues and water policy trends and consider if they may impact data centre usage, or profitability.

Show me the (government) incentive, I’ll show you the outcome

Incentives can make or break investment decisions. Malaysia offers tax holidays to attract data centre investments. Meanwhile, Indonesia facilitates faster permits and land acquisition processes. These incentives not only lure investors but also foster a competitive environment for data centre growth.

Developed economies like Australia, Japan, South Korea and Singapore are natural targets for data centre investment, with advanced economies, strong legal frameworks, high levels of international and domestic connectivity and talent density. Investors are extremely keen to allocate capital to those markets.

Other jurisdictions in the region therefore often work harder to attract capital. Governments in those jurisdictions are more likely to create investment incentives and regulatory settings designed to attract the capital, skills, technology and ecosystem needed to expand the domestic data centre market, including by offering:

- tax incentives such as reduced tax rates, tax exemptions, tax holidays or tax offsets for qualifying spending

- grants or subsidies for expenditure on data centre research, construction or operations

- discounts on rental and utility payments

- streamlined land access, zoning, permitting or utilities

- exemptions to foreign ownership controls for land or facilities, and

- relaxed immigration and visa requirements to attract a skilled workforce.

Incentive programs vary across the APAC region. However, there are a few common approaches: special economic zones and special status.

Building data centre ecosystems with Special Economic Zones (SEZs)

Across the region, industrial or high-tech parks are becoming enhanced into SEZs to encourage data centre investment. At their most basic, these SEZs provide access to the infrastructure and services needed for a data centre ecosystem including power, water, telecommunications and road infrastructure. However, government authorities may also offer incentives and benefits, such as those mentioned above.

Special status to attract targeted investments

Some incentives provide special status that is not linked to any specific zone or area.

Malaysia

Eligible data centre businesses in Malaysia can seek approval for ‘Malaysia Digital Status’. This provides access to a number of tax concessions, including income, investment and sales tax exemptions and allowances. Additionally, the Digital Ecosystem Acceleration Scheme (DESAC) provides other, separate capital allowances to apply against taxable income for data centre operators that meet certain criteria, such as local employment commitments and green technology deployments.

Singapore

‘Pioneer’ businesses that bring new technology can access income tax exemptions and reduced tax rates, and those who expand high-value infrastructure in Singapore can seek reduced corporate income tax rates as low as 5-10%.

Indonesia

Investments in the digital economy, including data processing and hosting activities, can qualify for a tax allowance under the Minister of Finance Regulation No. 130/PMK.010/2020. This incentive requires a minimum investment of IDR100 billion (~US$6.1 million).

Japan

As part of the government’s decentralisation efforts, subsidies are available for projects on ≥10 hectares of land, covering up to ¥15.54 billion (~US$108 million) to off-set infrastructure-related costs, and for up to ¥30 billion (~US$208 million) for both infrastructure and facility construction-related costs.

Vietnam

The Investment Support Fund (ISF) is designed to provide financial incentives for high-tech enterprises, including high-tech data centre developments and operations. The ISF offers annual expense support and initial investment cost support.

WHAT YOU NEED TO CONSIDER

- Consider (early) leveraging tax incentives, grants, subsidies and SEZ benefits.

- Assess whether structural needs to meet the requirements for an incentive (for example, a required site location) are practical and ultimately useful.

- Assess if there are any neutralising or negative factors of pursuing an incentive, including to compliance in other areas, other jurisdictions, or with other stakeholder expectations.

Understanding foreign investment controls

International capital is a critical driver of data centre growth in the APAC region. In emerging economies, particularly where domestic capital and expertise are limited, foreign investment is pivotal for delivering the digital infrastructure required to meet rising demand for data services.

It also supports broader economic goals - stimulating growth, digitising the economy, creating jobs, fostering innovation and bringing in expertise and advanced technologies that can improve operational efficiencies and service quality.

Governments across APAC increasingly recognise these benefits. Countries such as Vietnam, India and the Philippines are actively reforming or clarifying their regulatory frameworks to attract foreign capital and expertise.

Private capital, from global infrastructure funds to strategic investors, is also responding. With a strong appetite for risk-adjusted returns, these investors are targeting both mature markets with proven demand and emerging markets offering first-mover advantage.

In turn, this reinforces the pressure on governments to ensure their regulatory regimes support and enable foreign participation.

Diversity in regulation

Despite this trend toward liberalisation, foreign investment regulation across the APAC region remains highly diverse. Jurisdictions range from open and investor-friendly, to those with complex restrictions influenced by concerns around sectoral sensitivities, land ownership, national security and domestic industry protection.

The regulatory frameworks in place can either serve as a catalyst or barrier, influencing the scale and nature of investment in the region.

Finding the right pathway

The complexity of APAC’s regulatory landscape means foreign investment strategies must be carefully structured. Fragmented controls across land ownership, operating licences and critical infrastructure often require nuanced legal and commercial analysis and navigation. For example, in the Philippines, while 100% foreign ownership of data centres is allowed, foreign ownership of land is capped at 40% - though long-term leases are a permitted pathway.

This patchwork of regulation often leads foreign investors to pursue local partnerships or joint ventures, particularly in jurisdictions where:

- land ownership is restricted (for example, China, Thailand and Vietnam)

- operational licences are available to foreign investors, but land, infrastructure or telecommunications constraints apply (for example, Malaysia), or

- cultural sensitivities and business norms add complexity (for example, in South Korea and Japan, which remain quite local markets).

However, the benefits of local partnerships extend beyond compliance – they also include accelerated market entry, risk sharing and invaluable in-market insight.

Success for foreign investors in these markets often hinges on aligning with local partners, understanding layered regulatory regimes, and structuring investments that reflect both legal limits and market realities.

WHAT YOU NEED TO CONSIDER

- Consider (early) any relevant foreign ownership controls – these may apply to land, facilities, operations or even licences. Understand the triggers for approvals or notifications.

- Identify if local partnerships are required to navigate ownership restrictions.

- Align investment strategies with local norms and regulations to ensure compliance and optimise your market entry or expansion.

Local demand (not data localisation requirements) is driving investment onshore

Most jurisdictions have requirements to keep certain data onshore, or impose restrictions on data exports. This is common, for example, in relation to sensitive government data, financial information or health information. Some jurisdictions go further.

There is ample media and social commentary suggesting that data localisation measures are having the effect of driving data centre investment onshore in the jurisdictions where they are made.

The thesis behind this commentary is that cloud service providers and global technology companies cannot sustain a regional gateway model (servicing the APAC region from one jurisdiction or a small number of jurisdictions) if they must retain large amounts of data onshore, and therefore must construct data centres in-country to respond to capacity demands and other local requirements.

The survey of markets in this Guide revealed more nuance to this story, with impacted markets such as Vietnam and Indonesia having some of the world’s largest and fastest growing populations, it is more likely that market forces, in the form of increasing consumer demand for digital products and cloud services, are predominantly doing that work – with the help of government policies and regulations supporting foreign investment, digital transformation and infrastructure development.

However, this may change if AI sovereignty initiatives take hold (see Theme 8 below).

WHAT YOU NEED TO CONSIDER

- Monitor data localisation laws that could impact data centre operations.

- Focus on market-driven growth opportunities fuelled by increasing digital demand, rather than viewing data localisation as a business opportunity in itself. Map realistic local need.

- Assess if the policy and regulatory pipeline indicates an expansion, or contraction, of localisation rules to address sovereignty, capital attraction or other policy objectives.

Data centre growth is intertwined with export controls

Export controls are a reality for data centre investors. These regulations affect the availability of cutting-edge technologies, and they can delay projects. Investors must navigate these controls to ensure smooth operations and compliance.

The global expansion of data centres is being reshaped by AI export controls, given that most advanced AI chips and technologies are of US origin. Data centres also often use highly regulated commodities and/or 'dual use goods' which adds complexity.

Over time, but with a significant escalation in the past few years, the US has introduced sweeping restrictions on the export, re-export and transfer of advanced AI technologies aimed at safeguarding national security and preserving its technological lead in AI. These include:

- hardware controls on high-performance chips, and

- measures like the AI diffusion rule (though now rescinded), which sought to restrict access to powerful AI models trained on US technology.

These export controls have significant implications for data centre operators and investors in the APAC region, where access to cutting-edge AI hardware and infrastructure is critical to growth and competitiveness.

For now, many advanced AI technologies remain of US-origin, and export controls will continue to shape where and how data centres are built and operated across the APAC region.

Operators and investors must closely track regulatory developments and account for potential restrictions on chip access when planning infrastructure, particularly for AI-optimised or GPU-intensive facilities.

Navigating this shifting landscape underscores the need to stay agile - balancing geopolitical risks with the potential upside of rising local innovation and diversification.

WHAT YOU NEED TO CONSIDER

- Track ongoing developments in US export controls, especially concerning access to US-originating AI technology and controls on GPU-as-a-service models. This is a moving feast.

- Implement a strong trade compliance framework covering export controls, sanctions and dual-use goods, with alternative sourcing strategies to mitigate technology access restrictions.

- Craft tailored contractual protections that go beyond a duty to ‘comply with applicable law’ and address specific regulatory risks.

The data centre opportunity for national security and AI sovereignty

Data centres are strategic assets. They support national security and data sovereignty.

In Indonesia, the government is investing in data centres to ensure data sovereignty and boost its digital economy. Australia is focusing on securing its data centre infrastructure as part of its national security strategy. These moves underscore the critical role of data centres in safeguarding national interests.

Industry leaders and governments around the world are increasingly convinced that AI technology will be a lynchpin of economic success in the future, but there’s a lot of upfront investment required to reap the benefits.

Concerns are shaping government strategies

Given the competitive advantages that are expected from AI technology and the uncertainty in the global political and economic landscape, many governments are nervous about becoming reliant on AI infrastructure, large language models (LLMs) and products based overseas. This is due to:

- the potential limited access to the resources, and

- the risks associated with transferring to an overseas operator the necessary amount of sensitive domestic data to reap the benefits of the technology.

Taiwan and the Singapore-johor SEZ in Malaysia have tax concessions specifically introduced to bring in AI-related businesses. Other jurisdictions like australia are in the process of debating and implementing ai governance frameworks.

Data centre capacity is a key resource to achieve AI sovereignty goals. However, our anecdotal experience is that this focus on AI sovereignty seems to be manifesting at the level of policy rather than direct investments at this stage. Jurisdictions in the APAC region are at different levels of progression in their AI sovereignty strategies.

The inevitable rise of AI

McKinsey forecasts that demand for data centre capacity generally is likely to increase by around 22% year on year to 2030, putting total global demand in 2030 at roughly 3 times current demand. To meet that demand will require a significant increase in the rate at which new capacity is brought online.

AI-specific data centre capacity is expected to rise even faster - 33% year on year. Yet much of the existing data centre capacity is not capable of supporting the density of computing power demanded by AI without significant retrofitting and re-engineering of existing sites to meet the power and cooling demands that come with that intense computing.

Accordingly, AI-ready data centre capacity is an enticing investment opportunity in the region. Early movers may reap significant benefits if they can bring capacity to market to then fund further expansion throughout the region.

A key question for any AI sovereignty initiative is how it will be implemented. Currently, all of the top LLMs are either developed in the US or China. If sovereign AI capability is deployed using one of those LLMs – which may be a commercial and technical reality – that decision may come with geopolitical consequences, in much the same way as acquiring military hardware. Will AI sovereignty really be about political alignment to the US or China?

WHAT YOU NEED TO CONSIDER

- Consider impact of national security policies and regulations when planning data centre locations and operations.

- Stay informed with evolving government AI strategies and potential impacts on data centre needs, including new opportunities for investment in AI-ready infrastructure.

- Explore local opportunities or partnerships where foreign investment faces regulatory hurdles.

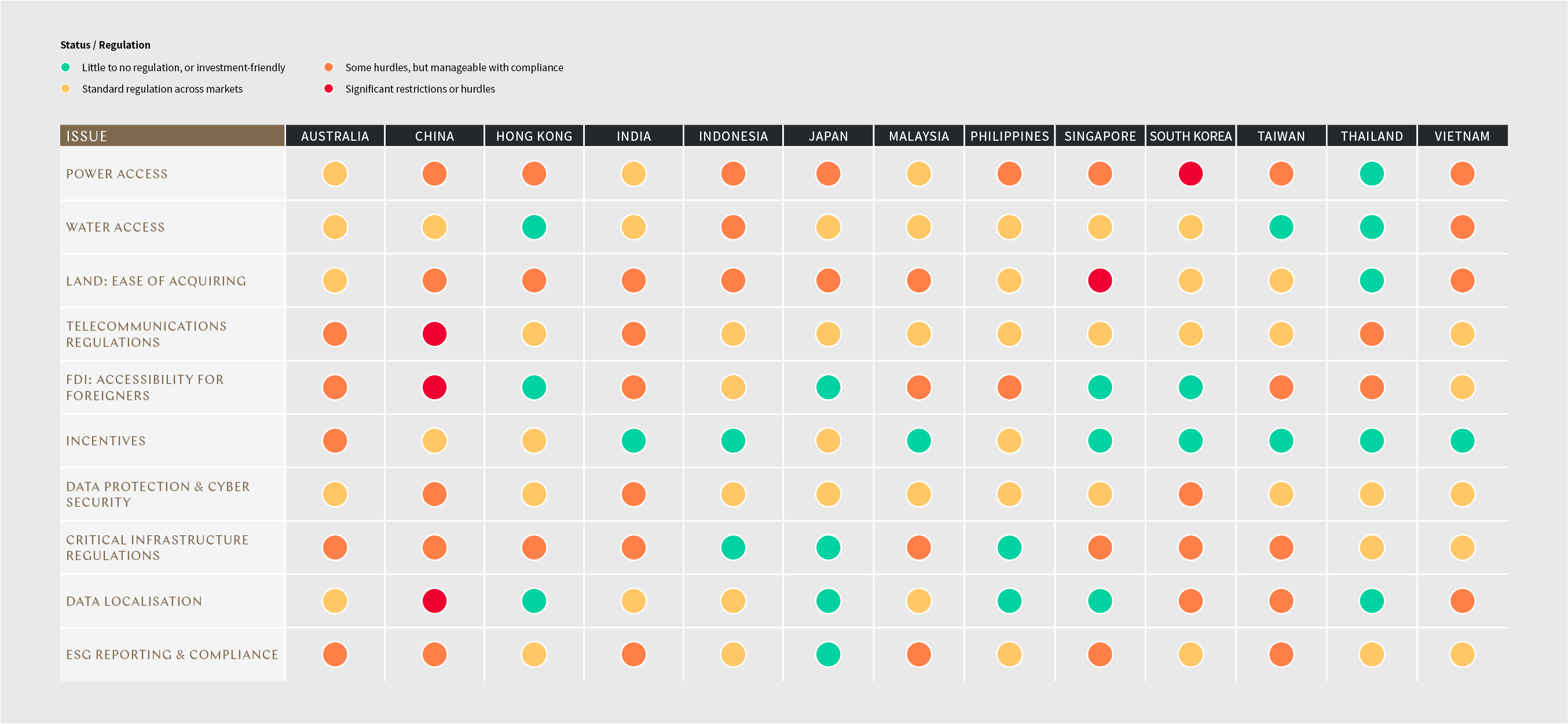

A regional snapshot

What does the regulatory landscape look like - in one heatmap? We've collated the settings captured throughout this Guide to give you a high-level view of how investor-friendly jurisdictions are across key issues - from very (little to no regulation), to not at all (significant regulatory restrictions).

What did we find?

Malaysia, India, Vietnam, and Indonesia present both opportunities and challenges. Thailand is emerging as an attractive location. Singapore and South Korea offer appealing incentives, tax benefits and supportive digital economy policies, offering more reliable investment decisions.

Conversely, regulatory nuances in areas like energy procurement, land acquisition and data localisation, especially in markets like China, can pose significant hurdles.

Click image to enlarge