In downtown Seoul, residents formally object to the construction of a new AI data centre – not in my backyard – swinging the sword of Damocles over the project.

In a data centre hub of Tokyo, a developer receives word from local power grid operator TEPCO: a site they’ve purchased to develop a data centre will not have the power it needs for up to 10 years.

Meanwhile in Singapore, after the lifting of a moratorium on new data centres between 2019 and 2022, data centre operators and their customers wait several years for the government to publish a ‘call for application’. This would open the chance to secure the right to build new data centres in the little red dot. They go over the border to Johor, Malaysia, instead.

These are real scenarios, highlighting the challenges of developing the nervous centres of our digital existence – data centres – where we need them. And they could be a sign of what’s to come for Australia.

Less than a year ago, in November 2024, the New South Wales government announced a ban on further data centre developments covering almost half of Macquarie Park, Sydney, one of Australia’s data centre hubs. The decision was aimed at fast-tracking new affordable housing close to transport, but it highlights the tension between sustainable urban development goals and digital infrastructure growth. The tension between competing - and critically important - government policies.

We’re supposed to be seizing the AI revolution, delivering what the CSIRO estimated as a $315 billion boost to Australia's GDP by 2030. Along with the productivity lift that flows from digitalisation.

To do that, we need data centres. Can we build them fast enough?

'AI could be the missing ingredient in the productivity equation which turns things around and returns the worlds advanced economies to stronger growth.'

- CSIRO Data61, AI Roadmap

The US$156bn growth challenge

An estimated US$156bn is needed to develop the data centre pipeline across APAC over the next five years - 1.7 times the capital the US will need.

Private capital is surging into data centres, which has risen to the second most-preferred alternative asset class based on CBRE’s 2025 Asia Pacific Investor Intentions Survey.

Blackstone’s $24bn acquisition of data centre provider AirTrunk in 2024 gave a glimpse of the magnitude of opportunities in the space. As did HMC Capital’s buyout of Global Switch Australia Data Centres and KKR and Singtel’s investment into ST Telemedia Global Data Centres the same year.

Escalating demand will keep deals coming and investors circling. Innovation will keep chipping away at challenges, from Australian operators investing in renewable energy and battery storage to new cooling technologies cutting water use.

That doesn't mean we can afford to take progress for granted - and assume that without building the support needed, the data centres will come.

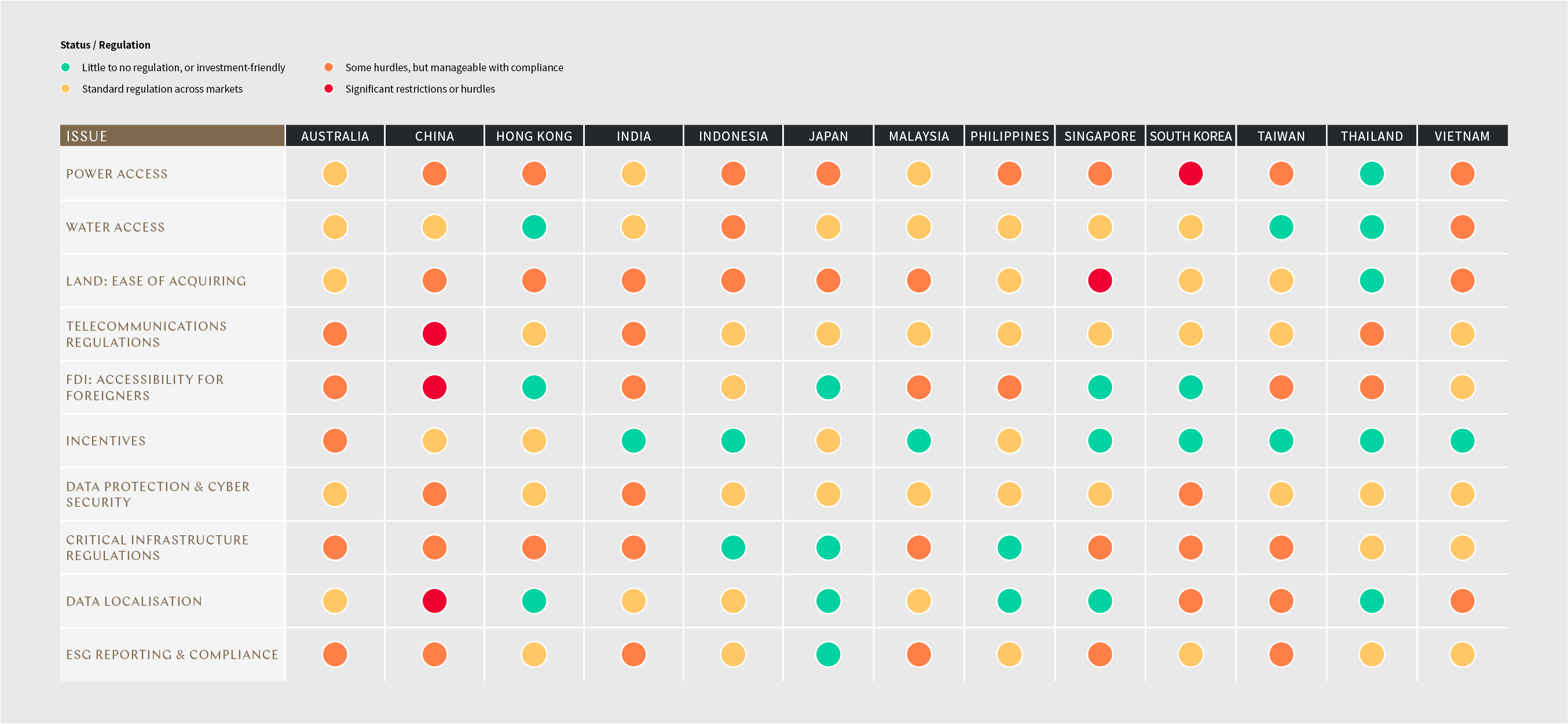

We worked with experts from across the region to dissect the regulatory settings and incentives that can make or break deals. What do you need to consider when approaching investment opportunities in the region? And what are the opportunities?

Discover what we found here: Navigating data centre opportunities across APAC - KWM.

There are real constraints and other issues in achieving that pipeline - the 'holy trinity' of land, power and water have long presented major hurdles. Larger data centres can use almost 25 Olympic swimming pools of water a day - a statistic that sits uncomfortably in a drought-stricken country like Australia, as it does in emerging hubs like Johor, Malaysia, where new developments are rejected on the basis of water availability.

As the need for data centres has grown, so too have the challenges - from foreign investment restrictions and export controls on advanced AI chips and technologies, to national security policies.

Developments bump up against competing priorities in a housing crisis. Community backlash feeds the growing need for a social licence. But this is the bargain we have for using the services data centres enable on a day-to-day basis.

Multifaceted challenges demand multifaceted responses

Across APAC, we see a mix of responses to these challenges. Our recent review of data centre regulations across the APAC region showed how our neighbours are setting incentives and introducing regulatory frameworks to meet the digitalisation demand. Some are moving data centres closer to power generation (South Korea). Others, to areas beyond their most concentrated cities (Japan). A number are vying for position as a regional data centre hub (like Johor, Malaysia), seeking ways to make the development process easier and more streamlined.

Australia failed to receive even one ‘green’ rating (the highest result) for investor-friendliness across ten key regulatory issues facing data centre developments.

Click to enlarge the chart

As data centres spread across Sydney, Melbourne, Perth and Brisbane, pushing further into suburban and regional areas, the imperative accelerates. We need to understand and address the fast-approaching issues on the horizon, before disjointed responses emerge. Federal, state and local governments, regulators, grid operators, water utilities, communities and others will have to come to the table to consider issues from a collective perspective.

There are positive signs. Just this month, Federal Treasurer Jim Chalmers opined on 'turning algorithms into opportunities’, by growing infrastructure investment to support AI as a force for good.

‘Next steps [include] helping to attract, streamline, speed‑up and coordinate investment in data infrastructure that’s in the national interest, in ways that are cost effective, sustainable and make the most of our advantages.’ Federal Treasurer Jim Chalmers, August 2025

What’s happening in our regional playground brings not only cautionary examples of what’s ahead for Australia, but invaluable lessons to help us seize opportunities – if we can look, listen and work together.

Discover the trends shaping tomorrow's markets. Stay ahead in Asia.