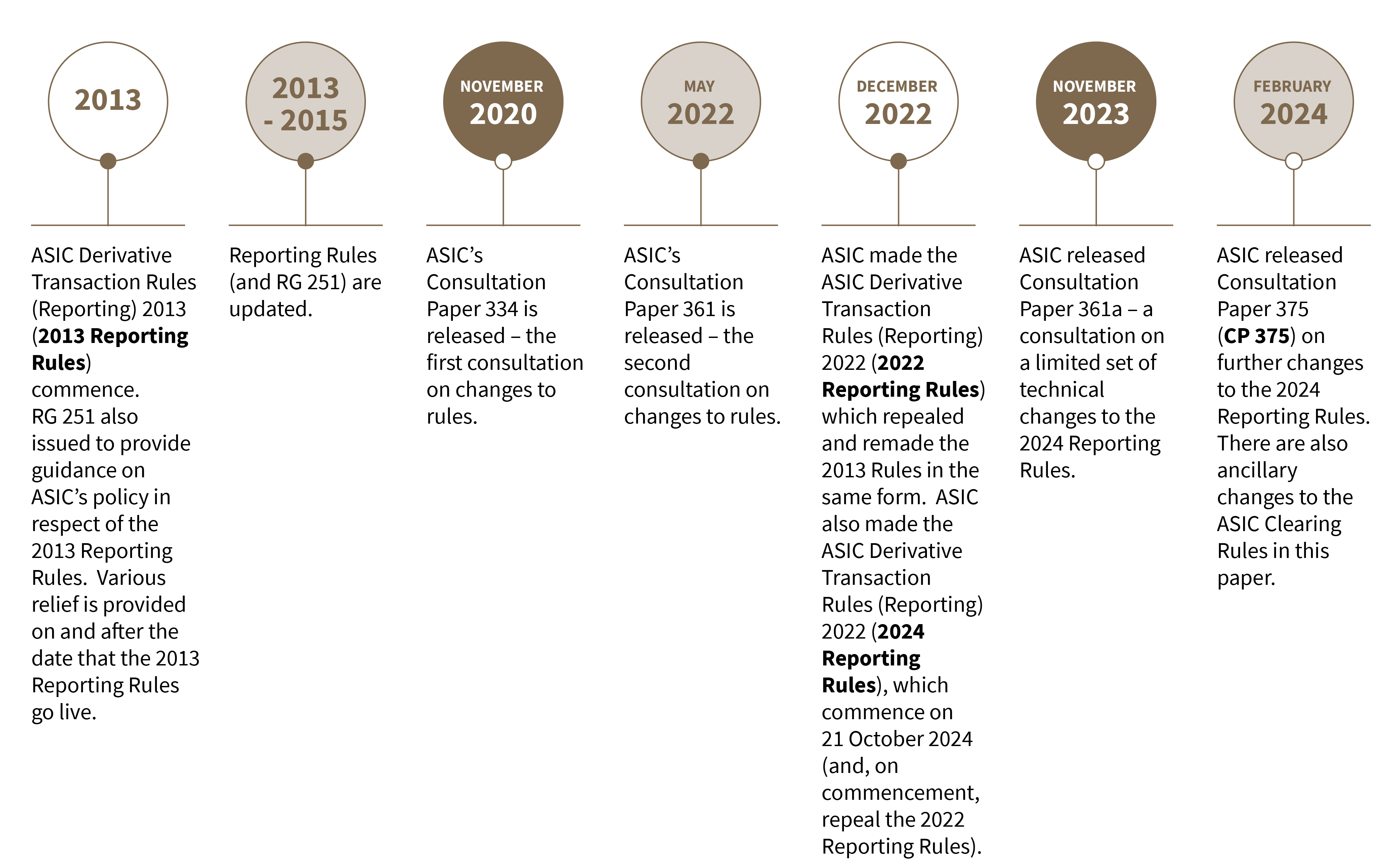

Over a decade ago, Australia introduced requirements to report information about OTC derivative transactions as part of its G20 derivatives reform commitments in the aftermath of the global financial crisis. The derivative transaction reporting rules made by ASIC establish these requirements in Australia. These rules were originally introduced in 2013 (ASIC Derivative Transaction Rules (Reporting) 2013) and were remade in 2022 (ASIC Derivative Transaction Rules (Reporting) 2022). These rules set out the requirements applicable to ‘Reporting Entities’ to report information about their OTC derivative transactions to licensed and prescribed repositories. Importantly, new rules (ASIC Derivative Transaction Rules (Reporting) 2024) are coming into force in October 2024. Now is the time to engage with the detail of the regime, and ensure that your legal, compliance, operational and technological processes are up to date, fit for purpose and consistent with these requirements.

Since the G20 made its derivatives reform commitments, a raft of laws and rules relating to derivatives trade reporting (and other regulatory requirements for derivatives) have been implemented in a wide number of jurisdictions. However, the information collected needs to be coordinated and consistent across international borders if it is to paint an accurate picture of the global OTC derivatives market.

Discrepancies and differences between the rulesets across jurisdictions have meant that regulators have access to different information depending on the requirements of their rules, and market participants often have to grapple with complying with differing requirements in different places. This has led to a set of complex, detailed and often prescriptive rulesets which are highly technical, both legally and operationally.

The trade reporting requirements imposed in various jurisdictions across the globe are now being adjusted in an attempt to improve and harmonise collected data. Five jurisdictions will implement revised rules in 2024 – Japan on 1 April, the EU on 29 April, the UK on 30 September, and Australia and Singapore on 21 October. However, differences will continue to exist.

As a result, it is crucial that market participants are aware of and understand the requirements which may apply to them in each relevant jurisdiction. In Australia, this includes understanding the current rules, the various exemptions and relief instruments which apply in certain circumstances, as well as the new rules which will come into force in October this year. Processes and procedures should be reviewed and updated to ensure compliance with both the current requirements and the new requirements. There are also substantial changes contained in the 2024 rules including both technical changes to the information which is required to be reported, as well as changes to the requirements of the rules and their application. Breaches of reporting rules can be serious and substantial penalties could apply and ASIC has repeatedly emphasised that one of the aims of amending the rules is to ensure improved data quality for Australian regulators.

ASIC has spent a considerable amount of time consulting on the upcoming 2024 rules, and is currently consulting on further amendments to be made to be implemented both in October 2024 and in April 2025. However, ASIC has not yet released a consultation on updates to Regulatory Guide 251: Derivative transaction reporting (RG 251) to accommodate the proposed changes in the 2024 Reporting Rules – RG 251 will provide important guidance to reporting entities on the requirements of the Australian derivative transaction reporting regime. It will be important for reporting entities to watch out for, and carefully consider, the consultation on updates to it.

A brief timeline of the implementation of the derivative reporting requirements is set out below.

ASIC’s latest consultation paper, CP 375 contains a number of important changes particularly for foreign reporting entities, as well as some other technical changes – it is available here. It also proposes some amendments to the ASIC Derivative Transaction Rules (Clearing) 2015 (Clearing Rules). The table below contains a high-level summary of these changes. The consultation closes on 28 March 2024.

If you would like some help considering the implications of these changes for your business or the trade reporting rules more generally, please reach out to us. We have been advising on these rules since the start and are here to help.

|

TOPIC

|

CURRENT REPORTING RULES

|

PROPOSED NEW REPORTING RULES

|

|

Amending the definition of Exchange-Traded Derivative (ETD) |

2022 Reporting Rules (and current form of 2024 Reporting Rules) refer to a Derivative not being an OTC Derivative (and therefore not reportable) if it is able to be traded on a Part 7.2A Market or a Regulated Foreign Market. This definition is supported by lists of financial markets set out by ASIC under a determination. There is also an option for entities to use an alternate definition of ETD on the conditions set out under ASIC Corporations (Derivative Transaction Reporting Exemption) Instrument 2015/844. |

2024 Reporting Rules to be amended to introduce:

Anticipated to commence on 21 October 2024. |

|

Clarifying the FX securities conversion transactions exemption |

The 2022 Reporting Rules does not include the FX securities conversion transactions exemption, which is instead provided under Exemption 9 of the ASIC Corporations (Derivative Transaction Reporting Exemption) Instrument 2005/844). The current form of 2024 Reporting Rules incorporate this exemption, with certain drafting amendments. |

A ‘reasonable belief’ qualification will be inserted into Rule 1.2.4(6) of the 2024 Reporting Rules to address a concern from industry relating to the standard of determining the purpose of the relevant transactions under this exemption. Anticipated to commence on 21 October 2024. |

|

Changing in-scope reportable transactions for foreign entities and CS facility licensees |

The 2022 Reporting Rules set out in-scope reportable transactions for foreign entities and include all OTC Derivatives:

Additionally the 2024 Reporting Rules include all OTC derivatives entered into with a Retail Client located in this jurisdiction. Alternatively, foreign entities can opt-in to rely on the ASIC Derivative Transaction Rules (Nexus Derivatives) Class Exemption 2015 to determine certain of their in-scope reportable transactions. |

ASIC proposes to amend the in-scope reportable transactions for foreign entities to include ‘All OTC Derivatives … that are a Nexus Derivative’ instead of OTC Derivatives ‘entered into by the Reporting Entity in this jurisdiction.’ ASIC’s proposed Nexus Derivative definition will adapt paragraph 9(a) of the ASIC Derivative Transaction Rules (Nexus Derivatives) Class Exemption 2015 and will replace ‘All OTC Derivatives … entered into by the Reporting Entity in this jurisdiction.’ The other limbs of the in-scope reportable transactions will remain unchanged. Consequential amendments would be made to exclude CS facility licensees from the operation of these amendments. CS facility licensees would be required to report ‘All OTC Derivatives entered into with an Australian Entity.’ Anticipated to commence on 1 April 2025. |

|

Removing alternative reporting |

Foreign Reporting Entities may be able to satisfy their reporting requirements under the 2022 Reporting Rules (and current form of 2024 Reporting Rules) where they report under a foreign jurisdiction’s substantially equivalent reporting requirements to a prescribed repository and ‘tag’ the information as having been reported under the ASIC rules. |

The alternative reporting mechanism will be removed from the 2024 Reporting Rules by removing the foreign entity exception and de-prescribing the currently prescribed repositories. These amendments would therefore require foreign Reporting Entities to commence reporting to a licensed trade repository in accordance with the 2024 Reporting Rules. Anticipated to commence on 1 April 2025. |

|

Changing certain reporting fields |

The Derivative Transaction Information requirements in the 2022 Reporting Rules (and current form of 2024 Reporting Rules):

|

‘PEXH’ will be added as an allowable value for ‘Other payment type’, but only for the use-case of cross-currency interest rate swaps and only as an optional allowable value. ‘CCPV’ (central counterparty valuation) will be added as an allowable value for ‘Valuation Method’ without any limitation on its use. ASIC set out its expectations on use of this field in CP 375, which will also be provided in further guidance. ASIC notes it is open to engaging with Reporting Entities who wish to switch from reporting their own valuations to reporting CCP valuations. Anticipated to commence on 21 October 2024. |

|

Amending the definition of ‘Clearing Derivative’ |

The Clearing Rules currently exclude exchange-traded derivatives from being a ‘Clearing Derivative’ (and therefore not subject to clearing requirements) by using a similar formulation of language as is used in the 2022 Reporting Rules (and current form of 2024 Reporting Rules). |

ASIC proposes to simplify the Clearing Rules by including a new limb into the definition of ‘Clearing Derivative’ to require that the derivative must be an ‘OTC Derivative’ defined in the 2024 Reporting Rules and making associated changes. Anticipated to commence on 21 October 2024. |