The Government today released details of late-breaking changes to Australia’s new ACCC mandatory notification regime – introducing new notification thresholds, filing triggers, and exemptions.

Some of these changes will apply to acquisitions that complete from 1 January 2026. Other changes will only apply to acquisitions that complete after 1 April 2026.

These are significant changes that provide greater clarity about the transactions that do and do not need to be notified under the new mandatory notification regime.

Key points:

Changes to apply from 1 January 2026

1. Amended notification thresholds for asset acquisitions

2. New and expanded exemptions for real estate, financing transactions and financial markets

3. New superannuation exemption for transfers of members’ benefits between superannuation entities and changes of trustees

Changes to apply from 1 April 2026

4. New notification triggers for share acquisitions that do not confer control

5. Additional new notification thresholds for asset acquisitions

New notification thresholds and filing triggers

The table below sets out a summary of the key changes and when they will take effect.

|

ISSUE

|

TRANSACTIONS COMPLETING BETWEEN 1 JANUARY – 1 APRIL 2026

|

TRANSACTIONS COMPLETING FROM 1 APRIL 2026

|

|

Changed thresholds for asset acquisitions |

Amended thresholds apply

|

Additional new thresholds to apply

|

|

|

*This value is the total consideration/market value of all shares and assets being acquired under the contract or arrangement for the asset acquisition. |

|

|

Changes to control test for acquisitions of shares, units, or interests in a managed investment scheme |

No change Only share acquisitions that result in sole or joint control will need to be notified. ‘Control’ means the capacity to determine the financial and operating policy of an entity – either alone or jointly with ‘associates’ (as defined in the Corporations Act 2001, with some amendments). |

New requirements to notify share acquisitions even if they do not result in control Acquisitions of shares will need to be notified - even if they do not result in control – if they meet any of the new ‘bright line’ tests set out below and satisfy the monetary thresholds for notification. The bright line tests in the table below are based on the ‘voting power’ of the acquirer group and its ‘associates’ (as defined in the Corporations Act 2001). |

Bright line tests for transactions completing from 1 April 2026

For transactions completing from 1 April 2026 and which meet the monetary thresholds:

|

PRE ACQUISITION VOTING POWER

|

POST ACQUISITION VOTING POWER

|

NOTIFIABLE ACQUISITION?

|

|

Up to 20%* |

More than 20%* |

Yes - if the target company is not a listed entity and has less than 50 members |

|

Up to 20% |

More than 20% |

Yes - if the target company is a listed entity or has more than 50 members and the acquirer already controlled the target prior to the acquisition |

|

Below 20% |

50% or more |

Yes - if the target company is a listed entity or has more than 50 members and the acquirer does not control the target either before or after the acquisition |

|

20% or more to 50%* |

50% or more* |

Yes |

|

*Note: Disregard the voting power of associates that only have “minority shareholder protection rights”. |

||

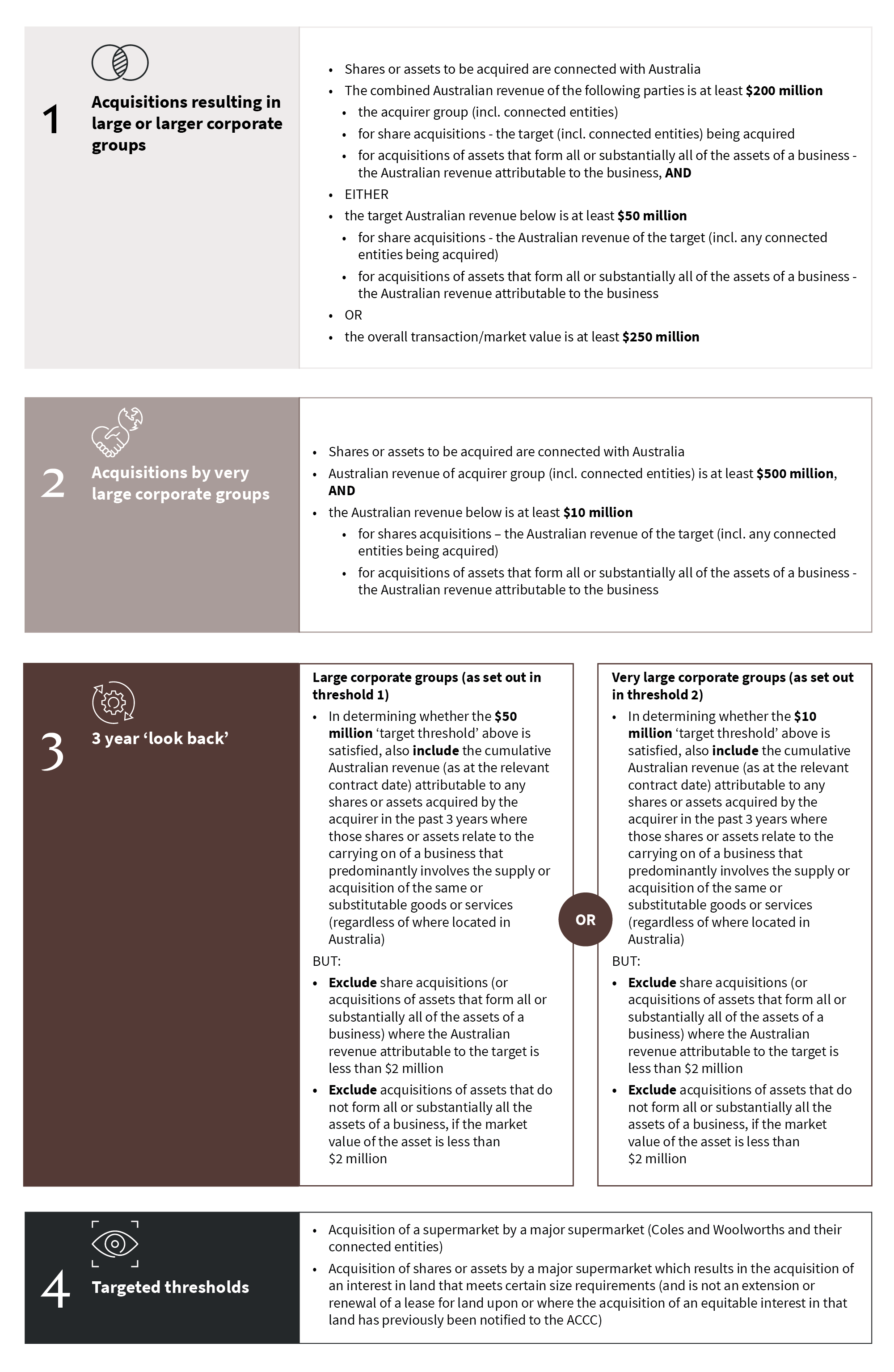

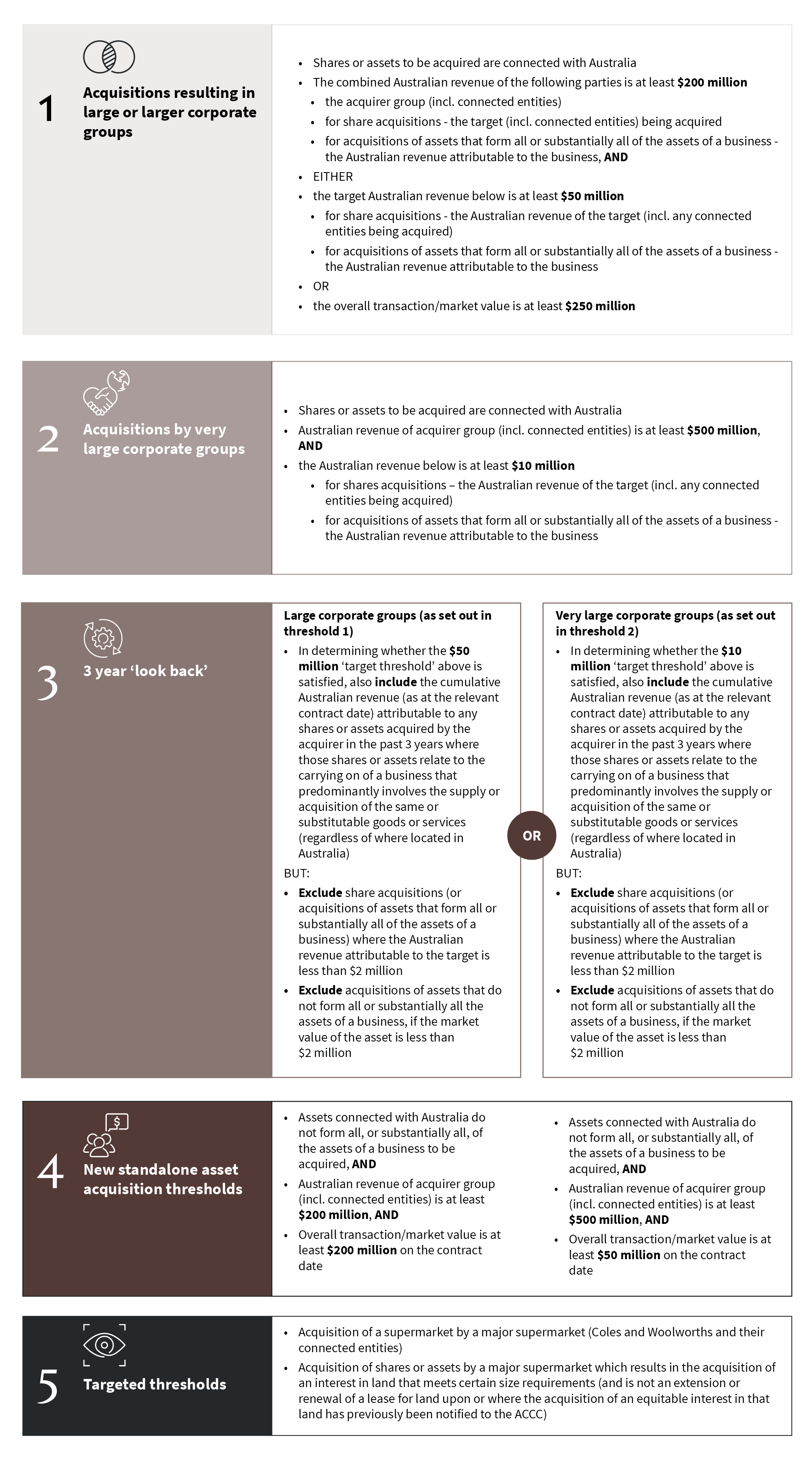

Further details in relation to the new notification thresholds are set out in Figures 1 and 2 below.

New and expanded exemptions for land, financial markets and superannuation

|

|

New and expanded exemptions for land, financial markets and superannuation

|

|

Land

|

Ordinary course of business A new exemption for acquisitions of equitable or legal interests in land applies if the acquisition is undertaken “in the ordinary course of business” (unless targeted thresholds apply – e.g. for supermarkets). The Explanatory Statement for the Amendment Determination (Explanatory Statement) indicates that the “ordinary course of business” is intended to capture routine acquisitions of legal and equitable interests in land – examples given include entering into an office lease, leasing a site to store inventory or manufacture products, acquiring an office tower for the purposes of commercial property investment, and property developers acquiring land to develop residential or commercial property. However, the Explanatory Statement also highlights a number of land acquisitions that would not be included within this exemption – examples given are acquisitions of land for the purposes of land-banking, land that a competitor is currently operating their business on or an acquisition involving the transfer of production or supply capacity from one competitor to another (e.g. a manufacturing business acquiring the lease of a direct competitor’s manufacturing facilities). Property development & quasi land rights

|

|

Financing transactions and financial markets

|

A number of exemptions applicable to financing transactions and financial markets have been updated and expanded to provide greater clarity following consultation with industry. These include changes to the exemptions that apply to financial market infrastructure, asset securitisation arrangements, derivatives, financial securities, debt instruments, money lending, financial accommodation, security interests (including credit support arrangements), and acquisitions of assets by specified external administrators. The Explanatory Statement provides helpful clarifications and explanations as to the intended policy objective and scope of these exemptions. |

|

Superannuation

|

A new exemption will apply to exempt acquisitions arising from transfers of members’ benefits between superannuation entities and changes of trustee. |

These exemptions (in particular, the financial market exemptions) are detailed and technical. Our experts in our Banking & Finance, Real Estate and Competition teams are ready to provide advice on the specific application of these exemptions.

Figure 1 - New notification thresholds – from 1 January 2026 to 31 March 2026

- All or substantially all assets of the business is not a defined concept. The Explanatory Statement provides that where the asset acquisition would enable the acquirer to effectively continue operating a business that is similar to the business currently operated using the acquired assets, this will typically involve an acquisition of all, or substantially all, of the assets of a business.

- Connected entity means an entity that is either a related entity of the first entity or is controlled by the first entity within the meaning of s50AA of the Corporations Act (with some amendments to 50AA(4))

- Australian revenue means the entity’s gross revenue (or the gross revenue of assets that constitute all or substantially all the assets of a business) - determined in accordance with accounting standards - for the entity’s most recently ended 12-month financial reporting period on the contract date that is attributable to transactions within or into Australia

- Transaction value means the greater of the sum of either (i) the consideration received or (ii) the market value of all the shares and assets being acquired pursuant to the contract, arrangement, or understanding pursuant to which the acquisition is to take place

- Connected with Australia means the body corporate (whose shares are to be acquired) or the entity in which the interest is acquired ‘carries on a business in’ - or that the asset being acquired is used in, or forms part of, a business carried on in Australia

- Contract date means the date on which a contract, arrangement or understanding has been entered into, pursuant to which the acquisition of shares or assets is to take place

Figure 2 - New notification thresholds – from 1 April 2026

- All or substantially all assets of the business is not a defined concept. The Explanatory Statement provides that where the asset acquisition would enable the acquirer to effectively continue operating a business that is similar to the business currently operated using the acquired assets, this will typically involve an acquisition of all, or substantially all, of the assets of a business.

- Connected entity means an entity that is either a related entity of the first entity or is controlled by the first entity within the meaning of s50AA of the Corporations Act (with some amendments to 50AA(4))

- Australian revenue means the entity’s gross revenue (or the gross revenue of assets that constitute all or substantially all the assets of a business) - determined in accordance with accounting standards - for the entity’s most recently ended 12-month financial reporting period on the contract date that is attributable to transactions within or into Australia

- Transaction value means the greater of the sum of either (i) the consideration received or (ii) the market value of all the shares and assets being acquired pursuant to the contract, arrangement, or understanding pursuant to which the acquisition is to take place

- Connected with Australia means the body corporate (whose shares are to be acquired) or the entity in which the interest is acquired ‘carries on a business in’ - or that the asset being acquired is used in, or forms part of, a business carried on in Australia

- Contract date means the date on which a contract, arrangement or understanding has been entered into, pursuant to which the acquisition of shares or assets is to take place