Why is this question important?

Being a director or officer (D&O) of a company is a role full of responsibility and associated risk. In the performance by a D&O of their duties, it is therefore a reasonable expectation that the company will safeguard them against litigation or investigation arising out of their conduct as D&Os. Equally, companies want to attract a high quality of D&Os. D&O Insurance plays a significant role in a company’s risk management and risk allocation strategy.

In addition to D&O Insurance, D&Os may be party to a deed of access and indemnity with the company or indemnified under the company’s constitution.

So, what does a D&O policy cover?

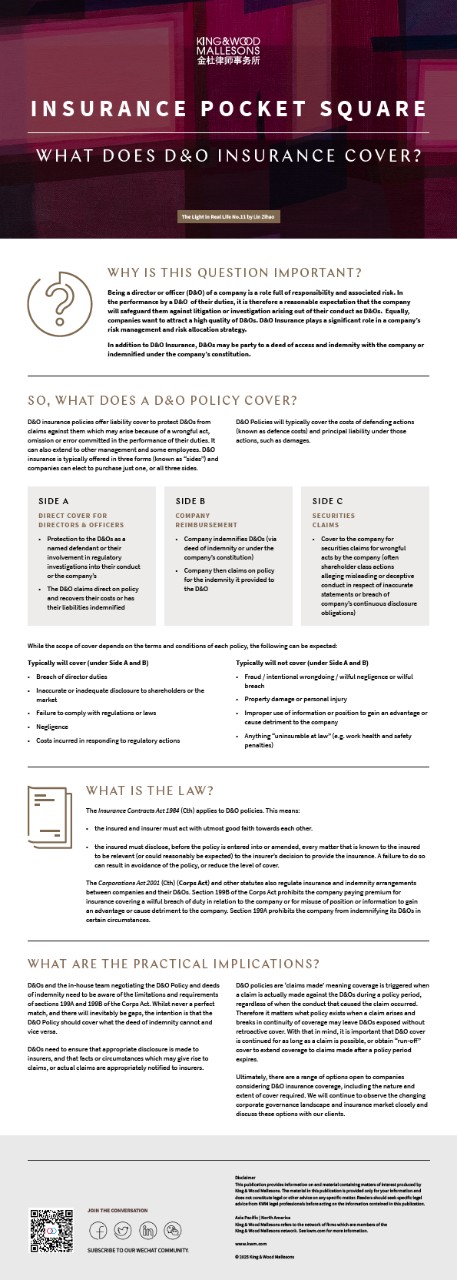

D&O insurance policies offer liability cover to protect D&Os from claims against them which may arise because of a wrongful act, omission or error committed in the performance of their duties. It can also extend to other management and some employees. D&O insurance is typically offered in three forms (known as “sides”) and companies can elect to purchase just one, or all three sides.

D&O Policies will typically cover the costs of defending actions (known as defence costs) and principal liability under those actions, such as damages.

|

Side A

|

Direct cover for directors & officers.

|

|

|

|

Side B

|

Company reimbursement

|

|

|

|

Side C

|

Securities claims

|

|

|

While the scope of cover depends on the terms and conditions of each policy, the following can be expected:

|

Typically will cover (under Side A and B)

|

|

|

|

|

Typically will not cover (under Side A and B)

|

|

|

|

What is the law?

The Insurance Contracts Act 1984 (Cth) applies to D&O policies. This means:

- the insured and insurer must act with utmost good faith towards each other.

- the insured must disclose, before the policy is entered into or amended, every matter that is known to the insured to be relevant (or could reasonably be expected) to the insurer’s decision to provide the insurance. A failure to do so can result in avoidance of the policy, or reduce the level of cover.

The Corporations Act 2001 (Cth) (Corps Act) and other statutes also regulate insurance and indemnity arrangements between companies and their D&Os. Section 199B of the Corps Act prohibits the company paying premium for insurance covering a wilful breach of duty in relation to the company or for misuse of position or information to gain an advantage or cause detriment to the company. Section 199A prohibits the company from indemnifying its D&Os in certain circumstances.

What are the practical implications?

D&Os and the in-house team negotiating the D&O Policy and deeds of indemnity need to be aware of the limitations and requirements of sections 199A and 199B of the Corps Act. Whilst never a perfect match and there will inevitably be gaps, the intention is that the D&O Policy should cover what the deed of indemnity cannot and vice versa.

D&Os need to ensure that appropriate disclosure is made to insurers, and that facts or circumstances which may give rise to claims, or actual claims are appropriately notified to insurers.

D&O policies are ‘claims made’ meaning coverage is triggered when a claim is actually made against the D&Os during a policy period, regardless of when the conduct that caused the claim occurred. Therefore it matters what policy exists when a claim arises and breaks in continuity of coverage may leave D&Os exposed without retroactive cover. With that in mind, it is important that D&O cover is continued for as long as a claim is possible, or obtain “run-off” cover to extend coverage to claims made after a policy period expires.

Ultimately, there are a range of options open to companies considering D&O insurance coverage, including the nature and extent of cover required. We will continue to observe the changing corporate governance landscape and insurance market closely and discuss these options with our clients.

Download

1.20MB, 1 Pages