On 18 March 2025, the Federal Court imposed a penalty of $10.5 million against Active Super finding that its environmental, social and governance (ESG) disclosure of its investment process made false and misleading representations in relation to certain investment screens and restrictions.

This is the latest in a series of significant penalties imposed against issuers found to have engaged in greenwashing activity, with the Federal Court also recently imposing a $11.3 million penalty on Mercer Superannuation (Australia) Limited and a $12.9 million penalty on Vanguard Investments Australia Limited.

In this alert, we consider an emerging trend of a simplified greenwashing test arising from recent Federal Court cases and ASIC’s ongoing scrutiny of ESG disclosures and what this might mean for you.

ASIC’s winning strikes on greenwashing

Recent greenwashing cases brought by ASIC against investment fund managers generally involved allegations that the relevant issuer made false or misleading representations about the ESG credentials of their investment products, such as excluding or restricting investments in certain industries or activities that pose a high ESG risk, such as gambling, tobacco, and fossil fuels.

In each of these cases:

- ASIC alleged that the defendants actually held investments, directly or indirectly, in companies that were involved in or derived profit from those industries or activities, contrary to issuer’s ESG claims;

- the Federal Court applied the well-established legal test for misleading or deceptive conduct, which is whether the conduct or representation would be likely to mislead an ordinary or reasonable member of the relevant class, being investors or prospective investors; and

- the Federal Court ultimately found that the defendants' representations were misleading and deceptive, or liable to mislead the public, in breach of sections 12DB(1)(a) and 12DF(1) of the ASIC Act.[1]

What is greenwashing?

In Australian Securities and Investment Commission v LGSS Pty Ltd [2024] FCA 587 (ASIC v Active Super), the Federal Court noted that some have traced first references to the concept of greenwashing as far back as 1986.[2] However, it is a concept that has come into sharp focus recently and has been noted by the Federal Court to mean:

“pertain[ing] to the misleading and deceptive disclosures employed by financial institutions to entice environmentally conscious investors into purchasing their financial products that, in reality, fall short of meeting the expected Environmental, Social, and Governance (ESG) or green credentials. These ESG credentials encompass environmental compliance and measures to protect the environment, reduce greenhouse gas emissions, and manage natural resources; social compliance, which evaluates how a company treats its stakeholders; and governance compliance, focusing on appropriate governance practices such as executive transparency and accountability.”[3]

Relevance to retail and wholesale vehicles

The tension is that documents in which greenwashing commonly occurs have an inherent marketing element and are, by definition, designed to entice investors to acquire the relevant product. Such documents include:

- an Information Memorandum or Private Placement Memorandum (typically utilised where the offering is to sophisticated / wholesale investors and not retail investors); and

- a Product Disclosure Statement (typically utilised where the offering is to retail investors).

However, such disclosure can extend beyond the above core disclosure documents, as demonstrated by ASIC v Active Super, where the misleading and false disclosure was held by the Federal Court to also relate to statements made in Active Super’s website and social media pages.

Relevantly:

- issuers must ensure that ESG statements made in any form of marketing are accurate, complete and verifiable in relation to their ESG practices. In particular, ensuring that the fund does not invest in securities or assets that are stated to be excluded investments under its ESG investment screening process , and clarifying whether the ESG restriction relates to direct investments or also indirect investments “down the chain”; and

- ASIC’s reliance on section 12DB(1)(a) and 12DF(1) of the ASIC Act to allege ESG representations as misleading and deceptive, or liable to mislead the public means that while ASIC’s recent focus has been on protecting retail consumers, court actions for greenwashing may technically be instigated irrespective of whether the claim pertains to marketing of an offer to retail investors or wholesale investors.

The pub test of ‘misleading and deceptive conduct’?

These recent cases indicate a shift in the courts’ approach to assessing misleading and deceptive conduct in relation to ESG disclosures.

Historically, the courts have adopted a higher threshold in misleading and deceptive cases which gave greater weight to the nature and content of the conduct, the circumstances in which it occurred, the characteristics of the relevant audience, and the effect or likely effect of the conduct on that audience. The courts have also traditionally recognised that some degree of generality or imprecision may be acceptable or unavoidable in certain types of disclosures, such as forecasts, opinions, predictions or statements of intention, as long as they are made honestly and on reasonable grounds.[4]

However, in the context of ESG statements, the Federal Court’s recent decisions are trending towards a more stringent and literal approach, focusing on the plain and ordinary meaning of the words or symbols used, and the impression they create in the mind of the ordinary and reasonable consumer.

In doing so, the Federal Court has also given less weight to any qualifications or limitations that may be contained in other documents or sources, such as other publicly available policy documents, external research, disclaimers, footnotes or hyperlinks, especially if they are not clearly or prominently displayed or communicated.

For example, in ASIC v Active Super, the Federal Court dismissed Active Super’s attempts to rely on qualifications found in a separate policy on the basis that when reading the policy as a whole, it was “farfetched and no ordinary reasonable consumer would have ever imagined [that Active Super was only promising] to use its best endeavours not to invest in gambling.”[5]

This approach may reflect the Federal Court's recognition of the growing significance and complexity of ESG issues and disclosures, and the need to protect investors who may rely on such disclosures in making their investment decisions – and therefore applying a more stringent and less sophisticated test in the context of ESG statements and greenwashing.

ASIC focus on ESG

The ability and willingness of our courts to engage with ESG-related issues has been fuelled by a ramping up of ASIC’s (and the ACCC’s) surveillance of ESG disclosures in the market.

ASIC has also signalled that funds and issuers are a particular focus. In remarks made to the Association of Superannuation Funds of Australia Conference in late 2024, ASIC Commissioner Simone Constant highlighted the need for superannuation trustees to improve oversight and transparency.[6]

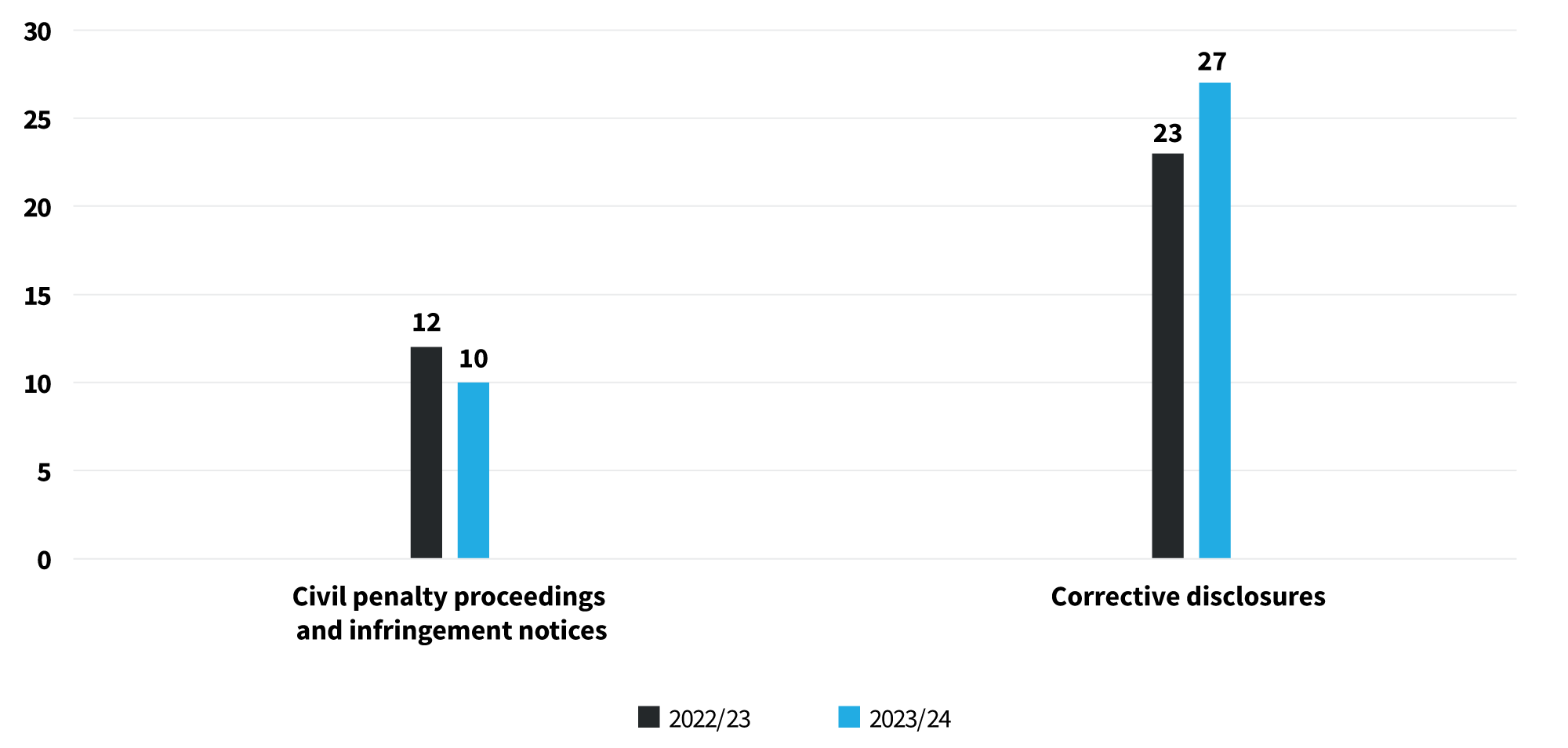

Image 1: Total ASIC civil penalty proceedings, infringement notices and corrective disclosures in relation to greenwashing matters

Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act).

Australian Securities and Investment Commission v LGSS Pty Ltd [2024] FCA 587 [1] (ASIC v Active Super).

Ibid [124].

See for example: Australian Competition and Consumer Commission v Dateline Imports Pty Ltd [2015] FCAFC 114 and Traderight (NSW) Pty Ltd v Bank of Queensland Ltd [2015] NSWCA 94.

ASIC v Active Super [121].

A detailed timeline of ASIC’s key activities over the past few years has been included at the bottom of this alert.

ASIC has indicated that it will continue to closely monitor:

- net zero statements and targets;

- use of terms such as “carbon neutral”, “clean” or “green”; and

- the scope and application of investment exclusions and screens.

Implications for issuers

Given ASIC’s increased and consistent focus on ESG claims and greenwashing and the Court’s more stringent test, issuers should therefore take steps to review and, if required, update their ESG disclosures and practices to ensure that they are accurate, complete and verifiable.

It is also critical to ensure that there is appropriate information sharing between those with oversight of the ESG and sustainability measures and those communicating with investors and prospective investors. It is also important that Boards and ESG committees ask questions and implement systems to ensure the effectiveness of these measures..

This may include for example ensuring that:

- all proposed investments, financial products and services are competently verified for consistency with any overarching claims made about the relevant ESG and sustainability strategies;

- bars are implemented to prevent investment in clearly excluded investments;

- regular portfolio reviews to ensure compliance with ESG representations;

- clear explanations are offered for investment exclusions or screening criteria, including proximate disclosure of any exceptions, qualifications, terms or thresholds used;

- broad, unsubstantiated sustainability-related statements or 'jargon' is avoided unless clearly defined or explained. ASIC has stated that terms such as ‘socially responsible', 'ethical investing' or 'impact investing' can mean different things to different people and issuers should take care to adequately explain such terminology in the relevant promotional material; and

- it is easy for investors to locate and access relevant information. In particular, in ASIC v Active Super, it was found by the Court that the reasonable consumer would not have had any reason to search through Active Super’s website for its “Sustainable and Responsible Investment Policy”. This case now acts as a warning to issues in relying on disclosure outside of the relevant disclosure document, particularly where “emphatic” statements are made upfront in relation to ESG exclusions and screenings.

Issuers should seek legal advice and assistance in relation to their ESG disclosure obligations and risks.

For legal advice in relation to your specific ESG disclosures, please contact a member of the King & Wood Mallesons team.

For advice to ensure that effective compliance measures are in place, please contact our regulatory compliance risk practice, Owl Advisory.

Timeline of ASIC's key greenwashing activities relating to issuers

|

Description

|

INDIVIDUAL

|

Example

uses 2

|

|

|

June 2022

|

ASIC released Information Sheet 271 which focused on sustainability-related products issued by funds. |

|

|

|

February 2023

|

ASIC initiated its first greenwashing civil penalty proceedings against Mercer Superannuation (Australia) Limited, alleging misleading statements about its Sustainable Plus investment options. |

|

|

|

March 2023

|

ASIC reported that between 1 July 2022 and 31 March 2023, its greenwashing interventions resulted in 23 total corrective disclosure, 11 infringement notices and 1 civil penalty proceeding. Its work during that time period included a surveillance of the managed funds sector, including a review of the PDSs of 122 funds, and further consideration of the investment processes of 17 funds. |

|

|

|

May 2023

|

ASIC issued an infringement notice to Future Super Investment Services Pty Ltd for overstating the positive environmental impact of the Future Super Fund in a Facebook post. This infringement notice was for $13,320. |

|

|

|

July 2023

|

ASIC commenced civil penalty proceedings against Vanguard Investments Australia Limited, alleging misleading claims about ESG exclusionary screens in their investment fund. |

|

|

|

August 2023

|

ASIC initiated civil penalty proceedings against LGSS Pty Ltd, trustee of Active Super, for misleading conduct and misrepresentations regarding its ESG investment practices. |

|

|

|

December 2023

|

ASIC issued infringement notices to Northern Trust Asset Management Australia Pty Ltd and Morningstar Investment Management Australia Limited for misleading statements about investment exclusions. |

|

|

|

February 2024

|

ASIC issues an infringement notice to Melbourne Securities Corporation Limited for misleading conduct related to investment exclusions in the Bloom Fund. The infringement notice was for $13,320. |

|

|

|

March 2024

|

The Federal Court found Vanguard guilty of making false or misleading representations about the ESG characteristics of the Vanguard Ethically Conscious Global Aggregate Bond Index Fund. |

|

|

|

June 2024

|

The Federal Court found that Active Super made misleading representations about its ESG credentials, investing in securities it claimed to have excluded. |

|

|

|

August 2024

|

The Federal Court ordered Mercer Superannuation (Australia) Limited to pay an $11.3 million penalty for making misleading statements about the sustainable nature of its investment options. |

|

|

|

August 2024

|

ASIC reported that between 1 April 2023 to 30 June 2024, its greenwashing interventions resulted in 2 civil penalty proceedings being commenced, 1 civil penalty proceeding being finalised, 8 infringement notices and 37 corrective disclosure outcomes. |

|

|

|

September 2024

|

The Federal Court imposed a $12.9 million penalty on Vanguard Investments Australia Limited for misleading claims about ESG exclusionary screens, marking the highest penalty for greenwashing conduct in Australia. |

|

|

|

March 2025

|

The Federal Court imposes a $10.5 million penalty on Active Super for greenwashing misconduct, following the June 2024 ruling. |

|

|